Our report is available below

Click the image to view/download the PDF

Market Insights

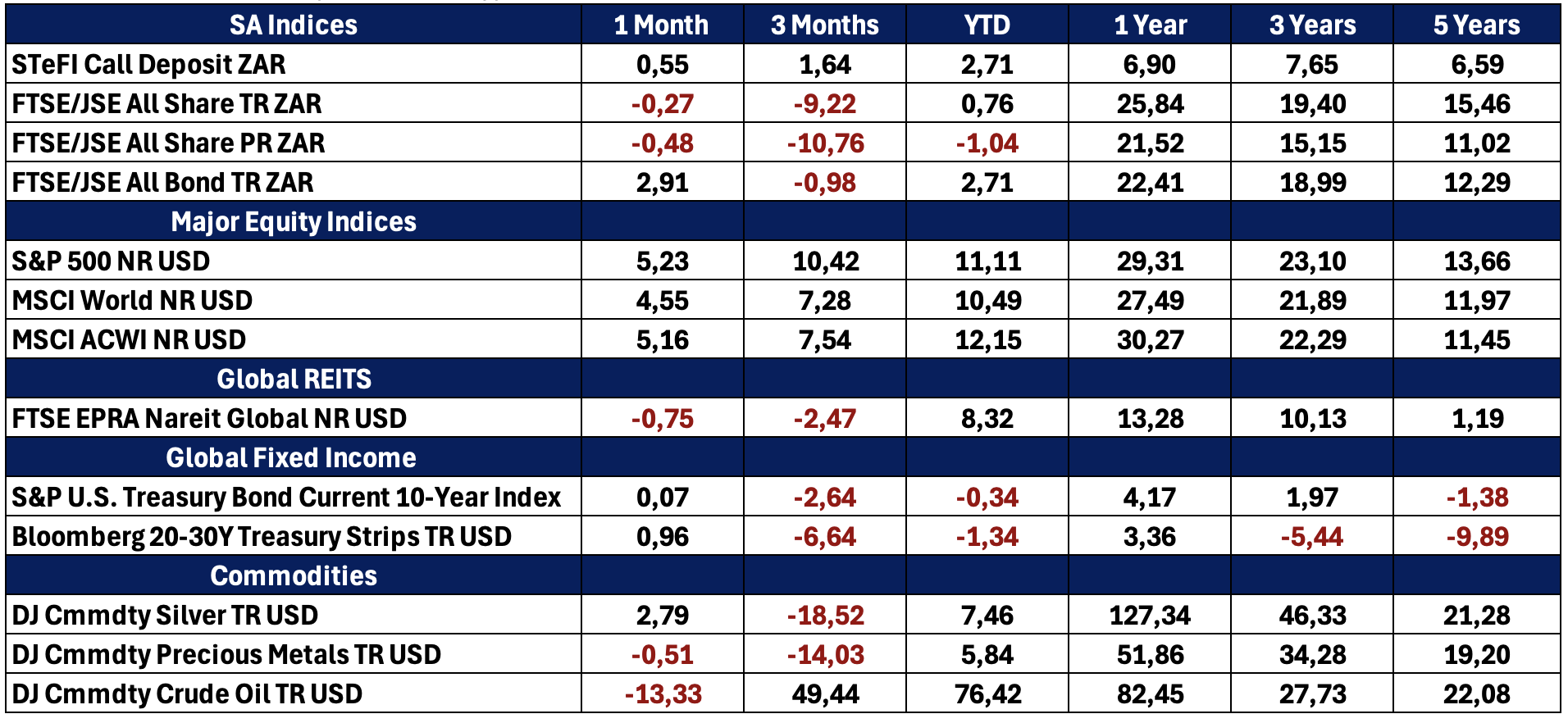

May 2026 extended the recovery that began in April, with global markets continuing to advance despite persistent geopolitical risks and elevated inflation pressures. The dominant narrative was one of resilient growth, strong earnings, and continued leadership from AI‑related sectors, even as central banks turned more cautious.

May 2026 extended the recovery that began in April, with global markets continuing to advance despite persistent geopolitical risks and elevated inflation pressures. The dominant narrative was one of resilient growth, strong earnings, and continued leadership from AI‑related sectors, even as central banks turned more cautious.

However, the rally became narrower and more selective, with leadership concentrated in large‑cap technology stocks. At the same time, falling oil prices late in the month provided some relief but came too late to prevent a notable re‑acceleration in inflation globally and locally.

In South Africa, inflation rose sharply to 4,0%, prompting the SARB to resume tightening, while the JSE lagged global markets, reflecting domestic and commodity‑linked challenges.

Global Markets – Equities: Gains Continue but Narrow

Global equities delivered another positive month, with major indices extending April’s rally with the S&P 500 returning 5,15% and the MSCI ACWI returning 5,21%. However, unlike April’s broad rally, May saw narrowing leadership with Large‑cap growth and technology stocks dominate, smaller companies and equal‑weighted indices lagged and market breadth weakened noticeably. This suggests that markets are becoming increasingly dependent on a concentrated set of AI‑driven winners, raising questions about sustainability.

The defining feature of equity markets remained AI‑linked growth with semiconductor and cloud infrastructure demand continued to surge. Earnings growth expectations were revised upward across sectors and the technology companies delivered exceptional results, with widespread earnings beats. AI‑related capex remains the central driver of earnings momentum, but dispersion between winners and losers widened significantly, highlighting increasing selectivity in markets.

Commodity markets saw a shift in May with oil prices declining significantly from April highs (down -13,93%) with the broader commodity indices falling by -7,61%, led by energy weakness. Despite the pullback, the earlier surge in oil continued feeding into inflation data keeping price pressures elevated globally and maintaining uncertainty around energy supply. Gold prices weakened, reflecting rising real yields and expectations of tighter monetary policy.

Central bank expectations shifted meaningfully in May, where rate cuts were largely priced out and the markets began pricing in potential rate hikes later in 2026, as inflation concerns dominated policy discussions. The Federal Reserve maintained a cautious stance, with policymakers highlighting, persistent inflation risk, uncertainty from geopolitical developments and limited scope for near‑term easing. The result is a clear shift toward a “higher‑for‑longer (and possibly higher)” interest rate environment.

Emerging Markets – Performance: Positive but More Selective

Emerging markets participated in the global rally but with less momentum than April when gains were more modest and uneven. Leadership remained concentrated in technology-heavy markets while commodity-linked and smaller emerging economies lagged. The broader theme is a transition from broad emerging market outperformance to a more differentiated environment.

Despite short-term variability, key EM drivers remain supportive. These include a strong earnings growth outlook, a central role in global AI supply chains and increasing resilience due to improved macro fundamentals. However, concentration risk remains elevated, particularly due to a reliance on a small number of large technology firms.

South Africa

South African Markets – Local Equities: Underperformance Continues

South African equities underperformed global peers with the JSE All Share declining slightly by -0,48% in May. This underperformance was driven by commodity price volatility, global growth concerns and domestic headwinds. This highlights South Africa’s continued sensitivity to global commodity cycles and external conditions.

The inflation dynamics shifted materially in May with CPI rising to 4,0% YoY in April, the Highest level seen in the past 2 years. The inflation print was driven primarily by fuel price increases. Additionally, core inflation increased to 3,6%, while producer inflation surged sharply to 4,80% due to rising input costs. This suggests that inflation pressures are broadening beyond energy, raising policy concerns.

In response to rising inflation, the SARB decided to raise the repo rate by 25bps to 7,00%, signaling concerns about second‑round inflation effects. Markets are now pricing in potential further rate hikes and a shift away from the earlier easing cycle, making this a significant pivot in South African monetary policy.

The rand demonstrated relative resilience, trading between R16,40 and R16,60 per US dollar during the month. This was supported by higher interest rate expectations and improved carry. However, volatility remained elevated and movements were largely driven by global factors such as oil, the US dollar and geopolitics.

Special Themes and Policy Watch

Market Narrowing and Concentration Risk

The most important shift in May was the narrowing of equity market leadership with the rally increasingly dependent on a handful of mega‑cap tech stocks and reduced participation from broader market segments. This raises risks around valuation concentration and potential volatility if leadership falters.

Transition from Disinflation to Inflation Pressure

The earlier disinflation trend has clearly reversed. Energy shocks have contributed to broader price pressures resulting in rising global and local inflation expectations. This creates a more challenging macroeconomic environment with slower growth potential and greater policy uncertainty.

Central Bank Pivot: From Cuts to Hikes

Markets have undergone a significant repricing of interest rate expectations with rate cuts being pushed out and increasing probability of further tightening. This has major implications for valuations, bond markets and currency dynamics.

South Africa: External Shock Transmission

May highlighted South Africa’s exposure to global dynamics with fuel-linked inflation shocks rapidly feeding into the CPI and prompting a proactive monetary policy response. Despite this, the economy demonstrates resilience supported by anchored expectations and a stronger currency than in previous cycles.

Looking Ahead

Key themes to monitor going forward:

- Inflation trajectory — whether pressures broaden further beyond energy

- Central bank actions, particularly potential rate hikes

- Oil price stability and Middle East developments

- Sustainability of the AI‑led equity rally

- South Africa’s ability to manage inflation without derailing growth

Closing Remarks

May 2026 reinforced the idea that markets can continue to rise even in a more challenging macro environment, provided earnings remain strong. However, the underlying conditions are becoming more complex as inflation is rising again, monetary policy is tightening and market leadership is narrowing. This creates a more fragile and selective investment environment, where active positioning and diversification will be increasingly important.

The Iza Portfolios

IZA Global Balanced Fund

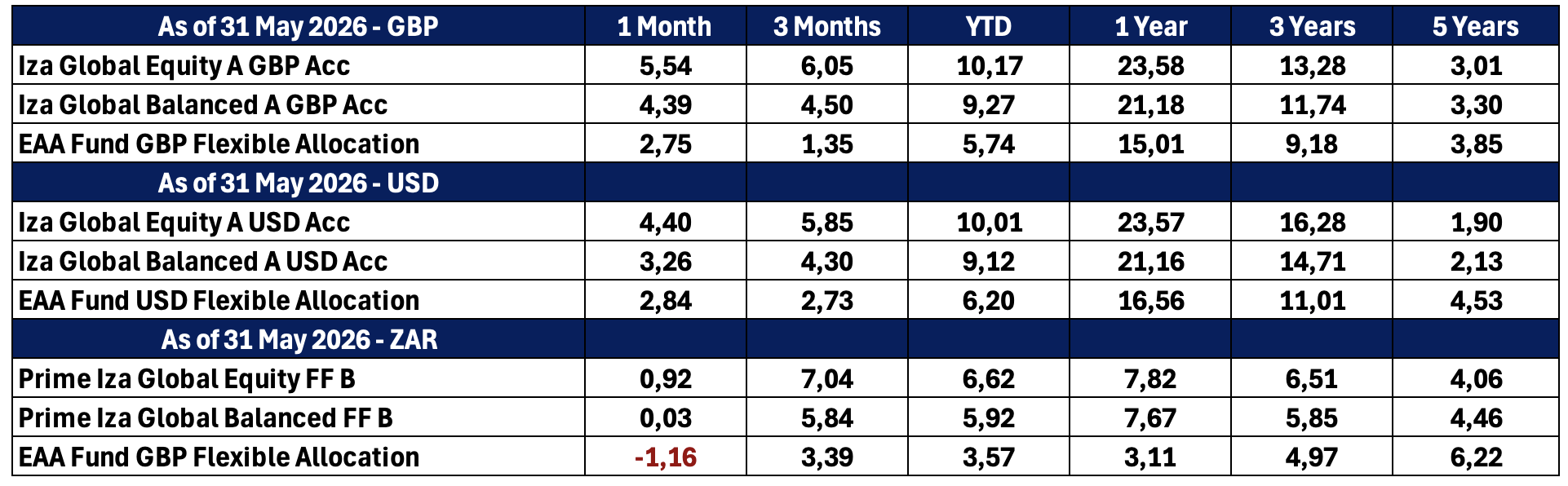

The Iza Global Balanced Fund delivered a solid performance in April 2026, returning 6.07% (GBP) and 9,09% (USD), recovering from the drawdown in March and lifting the year-to-date returns to 4.67% (GBP) and 5,67% (USD). The Iza Global Balanced Fund outperformed its peer benchmarks, the EAA GBP Flexible Allocation and the EAA USD Flexible Allocation, with the fund returning 6,07% (GBP) and 9,09% (USD) vs the peer benchmark of 3,59% (GBP) and 5,15% (USD) in April. This reflects the strong relative performance due to diversification, multi-asset positioning and manager selection.

April’s performance was driven by a broad recovery in risk assets, with equities and selected growth exposures leading gains. Scottish Mortgage was the standout performer for April, benefiting from a rebound in global growth equities and producing a return of 18,39% and contributing 1,40% to the portfolio. T.Rowe Price Global Focused Growth Equity Fund delivered a strong return for the month of April at 13,66%, contributing strongly with 1,03% to the portfolio. The Templeton Emerging Markets Fund had a meaningful rebound in April, with a return of 10,89%, reflecting the meaningful recovery in emerging market equities from March. The iShares MSCI World GBP and Jupiter Merian Global Equity Fund also supported returns producing a return of 9,25% and 7,71% respectively, while contributing 0,44% and 0,55% to the portfolio. Gold was the largest detractor of the portfolio, returning a -4,27% and detractive -0,19% from the portfolio. Our allocation to structured notes within the portfolio produce relatively muted returns for April.

Iza Global Equity Fund

The Iza Global Equity Fund delivered another strong month of performance in May 2026, returning 5,54% (GBP) and 4,40% (USD), and extending its year-to-date return to 10,17% (GBP) and 10,01% (USD). This marks a second consecutive month of strong gains, building on April’s rebound, as global equity markets continued to recover following the volatility experienced in March. The fund just underperformed the MSCI ACWI Index, which returned 6,01% (GBP) and 5,16% (USD) in May. Overall, the Fund continued to demonstrate solid absolute returns with broadly competitive relative performance.

Performance in May remained driven by global equity strength, particularly in growth and emerging market segments. The Templeton Emerging Markets remained the standout performer, providing a month end return of 14,98%, benefiting from continued strength in emerging markets. The continued strength in the global growth stocks and strong stock selection drove a solid return of 9,58% from the T.Rowe Price Global Focused Growth Equity Fund. Scottish Mortgage continued its sustained recovery with a positive return of 7,94%, driven by the positive SpaceX IPO noise. Our core holding the iShares MSCI World produced a solid return of 5,60%.

The Templeton Emerging Markets Fund was the top contributor to performance in May, with a strong 1,27%, along with T.Rowe Price solidly contributing 0,77% to the fund. Our core holding in the iShares MSCI World was the second significant contributor, providing a return of 0,87%, with Jupiter World Equity Fund coming in slightly behind with a contribution of 0,68%.

In summary the fund delivered a second consecutive month of strong positive returns, reflecting supportive global equity markets. Overall Performance was driven by growth-oriented and emerging market exposures, which continued to outperform. The Fund maintained strong absolute performance with competitive benchmark-relative results. Overall, the fund remains well positioned to participate in global equity upside, supported by its diversified multi-manager approach and effective allocation to high-conviction strategies. We continue to model and monitor the positioning of the fund as we navigate through this volatile and evolving market.

Quote of the month

Successful investing is about managing risk, not avoiding it.

Benjamin Graham

Funds’ Performance Summary

Asset Class Performance (Base Currency)