Our report is available below

Click the image to view/download the PDF

Market Insights

April 2026 marked a strong rebound in global markets following the sharp risk‑off correction in March. While geopolitical tensions in the Middle East remained unresolved and energy prices stayed elevated, investor sentiment improved materially, driven by resilient earnings, renewed enthusiasm around AI, and intermittent ceasefire optimism.

April 2026 marked a strong rebound in global markets following the sharp risk‑off correction in March. While geopolitical tensions in the Middle East remained unresolved and energy prices stayed elevated, investor sentiment improved materially, driven by resilient earnings, renewed enthusiasm around AI, and intermittent ceasefire optimism.

Global equities delivered their strongest monthly gains in years, with several indices reaching new all‑time highs. Emerging markets were standout performers, recovering losses and extending their year‑to‑date leadership.

In South Africa, markets remained volatile but stable overall. Inflation edged slightly higher, the rand fluctuated in response to global risk sentiment, and the JSE experienced mixed performance amid shifting commodity prices and global uncertainty.

Global Markets – Powerful Recovery and New Highs

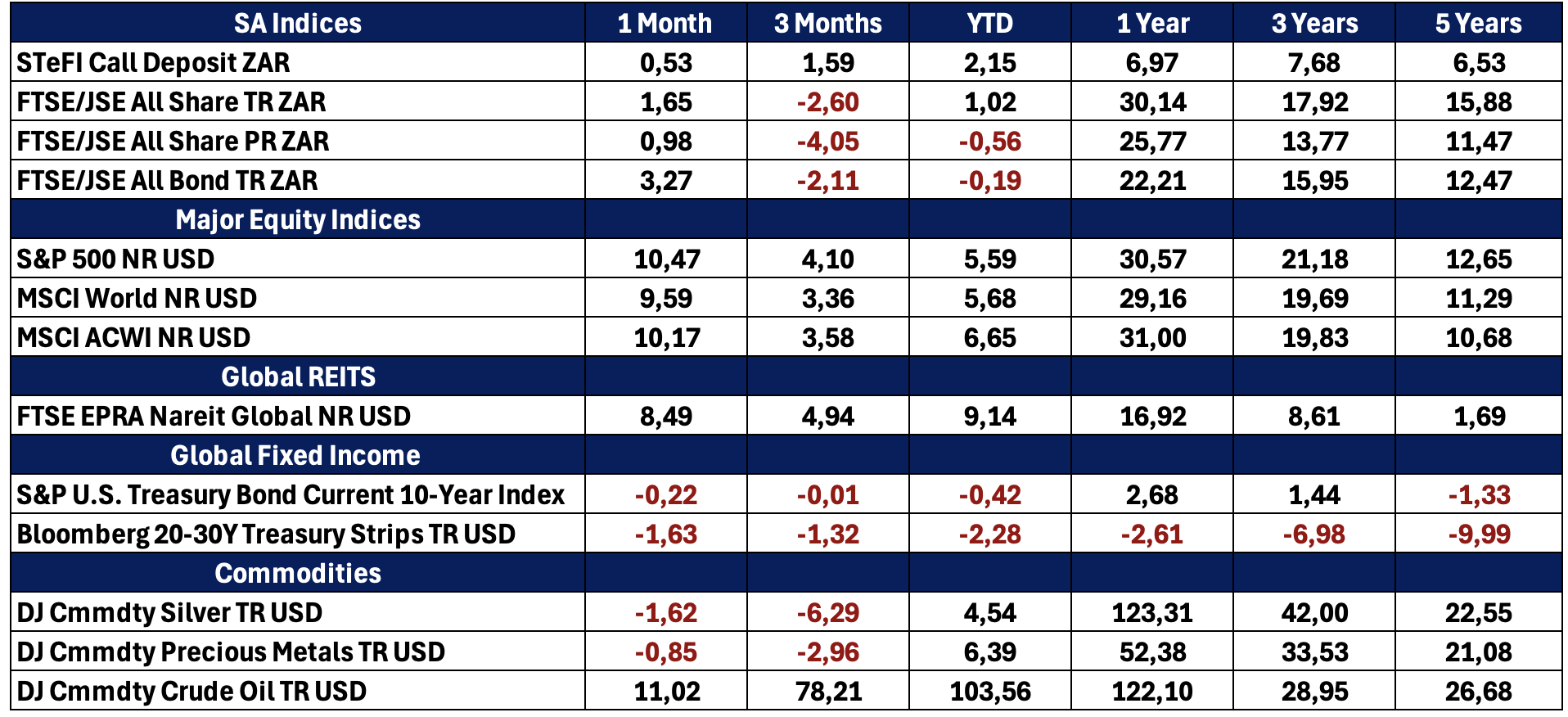

Global equity markets staged a strong risk‑on rally in April, reversing much of March’s sell‑off. The MSCI World Index rose nearly 10%, marking its strongest monthly gain since 2020, while U.S. indices such as the S&P 500 up 10,42% and Nasdaq up 15,29% reaching record highs.

Growth equities led the rebound, particularly technology and AI‑related sectors. The semiconductor index surged dramatically, reflecting continued investor conviction in AI‑driven structural growth. Importantly, markets appeared increasingly willing to look through geopolitical risk, focusing instead on earnings resilience and long‑term growth trends.

Oil prices remained a central theme. Despite brief declines early in the month on ceasefire hopes, Brent crude revisited highs above $110–$125 per barrel, underscoring the persistence of supply disruptions linked to the Strait of Hormuz. This sustained energy shock continued to: support commodity markets broadly, reinforce inflation concerns globally, maintain pressure on central banks.

Meanwhile, gold posted modest declines as higher real yields reduced its relative appeal, demonstrating a shift away from defensive positioning as risk appetite improved.

Central banks remained cautious in April. The U.S. Federal Reserve held rates steady at 3.75%, reinforcing a “higher‑for‑longer” stance amid persistent inflation and geopolitical uncertainty. Notably, the April meeting revealed unusual internal division, with a significant number of dissenting votes, the highest since the early 1990s, highlighting uncertainty around the policy path. Markets have now largely pushed out expectations for rate cuts, with inflation risks, particularly those linked to energy, complicating the path toward easing.

Emerging Markets – A Strong Rebound Led by AI Supply Chains

Emerging markets delivered an exceptional rebound in April, following March’s sharp decline. The MSCI Emerging Markets Index rose sharply to 14,53%, reaching new highs and outperforming developed markets. Performance was highly concentrated: Taiwan and South Korea surged due to semiconductor demand, AI‑linked manufacturing remained the dominant growth driver, earnings upgrades for EM companies exceeded those of developed markets. In fact, EM Asia indices recorded some of their strongest monthly gains in decades, driven by substantial capital expenditure and demand in AI infrastructure.

A notable theme emerging in April is how EM exposure is becoming increasingly concentrated in a small number of large semiconductor and technology firms. This raises important considerations for diversification and portfolio construction.

South Africa

South African Markets – Volatility Persists Amid Global Uncertainty

South African markets remained sensitive to global developments, particularly oil prices and geopolitical risk. The JSE traded unevenly, with declines in some sectors (notably basic materials) and recovery attempts later in the month. Business confidence weakened as global uncertainty filtered into local markets. Despite this, the market showed resilience relative to March’s sharp declines, supported by stabilising global sentiment.

Inflation dynamics began to shift with CPI rising modestly to 3,1% YoY. The full impact of higher fuel prices is expected to push inflation closer to 4% in Q2 2026. The increase reflects early transmission of global energy shocks into domestic prices, particularly via fuel and transport costs.

The Rand experienced notable volatility, weakening toward R16,60/$ during the periods of risk aversion and strengthened intermittently on improved sentiment and ceasefire optimism. The movements were largely externally driven, with oil prices and global risk appetite dominating currency behaviour.

Special Themes and Policy Watch

Markets Decouple from Geopolitics

Perhaps the defining feature of April was markets’ ability to rally despite ongoing conflict. While energy markets remained tightly linked to geopolitical developments, equities increasingly focused on earnings and structural growth themes.

AI Reasserts Market Leadership

AI‑related sectors regained clear leadership, strong earnings and capital‑expenditure signals, concentrated performance in semiconductor supply chains, and renewed appetite for “growth” over “defensive” positioning. This reinforces AI as a defining investment theme of 2026.

Inflation Risks Remain Elevated

While markets recovered, the macro backdrop remains challenging, Oil‑driven inflation persists, central banks face limited room to ease, and the risk of “higher‑for‑longer” rates has increased. The IMF highlighted that global growth may slow while inflation rises in 2026, a classic stagflationary risk scenario.

South Africa: Resilience with External Vulnerabilities

South Africa continues to benefit from, anchored inflation expectations, and positive real yields. However, vulnerabilities remain, heavy reliance on imported energy and sensitivity to global capital flows and commodity prices.

Looking Ahead

Key themes for May and beyond include:

- Trajectory of the Middle East conflict and energy supply stability

- Whether inflation pressures broaden beyond energy

- Central bank signalling amid rising uncertainty

- Sustainability of the AI‑driven equity rally

For emerging markets and South Africa, external factors, particularly oil and global liquidity conditions, will remain critical.

Closing Remarks

April 2026 demonstrated that markets can recover rapidly, even in the face of significant geopolitical disruption.

While risks remain elevated, investor focus has shifted back toward earnings strength, structural growth opportunities, and technological transformation. At the same time, the persistence of inflation and geopolitical uncertainty suggests that volatility is likely to remain a feature of markets in the months ahead.

A disciplined, diversified investment approach remains essential in navigating this evolving landscape.

The Iza Portfolios

IZA Global Balanced Fund

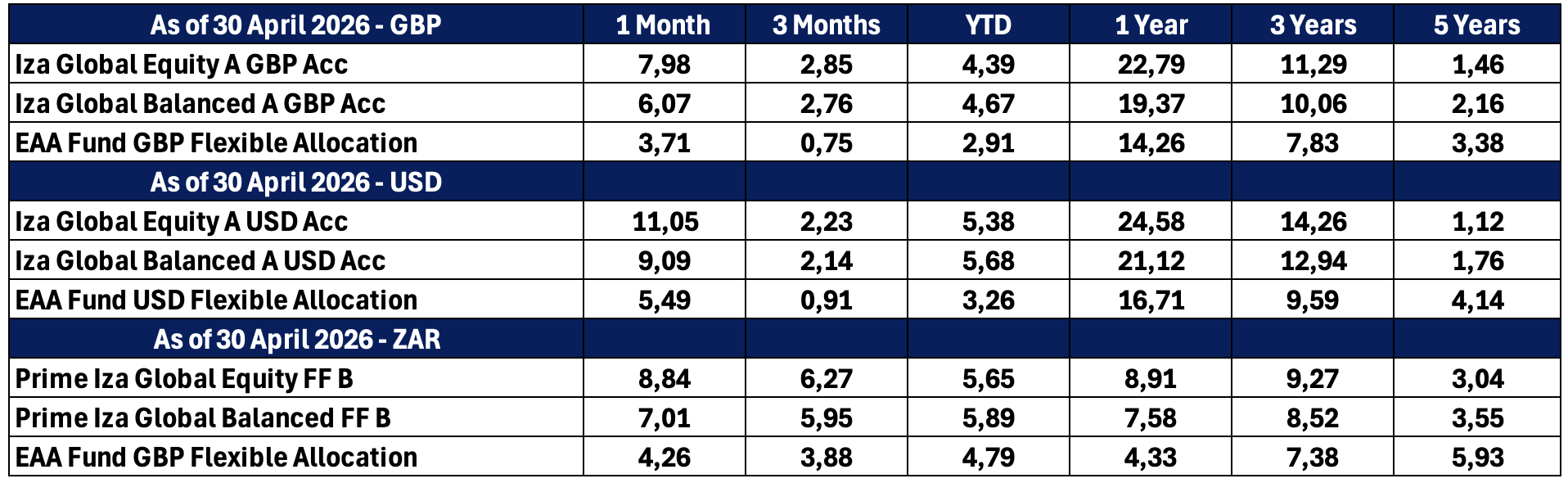

The Iza Global Balanced Fund delivered a solid performance in April 2026, returning 6.07% (GBP) and 9,09% (USD), recovering from the drawdown in March and lifting the year-to-date returns to 4.67% (GBP) and 5,67% (USD). The Iza Global Balanced Fund outperformed its peer benchmarks, the EAA GBP Flexible Allocation and the EAA USD Flexible Allocation, with the fund returning 6,07% (GBP) and 9,09% (USD) vs the peer benchmark of 3,59% (GBP) and 5,15% (USD) in April. This reflects the strong relative performance due to diversification, multi-asset positioning and manager selection.

April’s performance was driven by a broad recovery in risk assets, with equities and selected growth exposures leading gains. Scottish Mortgage was the standout performer for April, benefiting from a rebound in global growth equities and producing a return of 18,39% and contributing 1,40% to the portfolio. T.Rowe Price Global Focused Growth Equity Fund delivered a strong return for the month of April at 13,66%, contributing strongly with 1,03% to the portfolio. The Templeton Emerging Markets Fund had a meaningful rebound in April, with a return of 10,89%, reflecting the meaningful recovery in emerging market equities from March. The iShares MSCI World GBP and Jupiter Merian Global Equity Fund also supported returns producing a return of 9,25% and 7,71% respectively, while contributing 0,44% and 0,55% to the portfolio. Gold was the largest detractor of the portfolio, returning a -4,27% and detractive -0,19% from the portfolio. Our allocation to structured notes within the portfolio produce relatively muted returns for April.

In summary April saw a strong recovery, with the Iza Global Balanced Fund delivering robust performance. The fund outperformed its benchmark, driven by effective exposure to global equities. Growth and emerging market assets led gains, while defensive holdings lagged. The diversified structure tempered volatility, resulting in slightly lower return than pure equity strategies but more balanced risk exposure. We continue to carefully model and monitor the asset allocation positioning of the fund in the face of increasingly expensive, yet growth driven markets.

Iza Global Equity Fund

The Iza Global Equity Fund delivered a strong rebound in April 2026, generating a return of 7,98% (GBP) and 11,05% (USD), recovering sharply from the drawdown experienced in March and bringing year-to-date performance to 4.38% (GBP) and 5,38% (USD), slightly lagging behind the MSCI ACWI at 4,82% (GBP) and 5,90% (USD). In the month of April the Iza Global Equity Fund outperformed the MSCI ACWI, with the Iza Global Equity Fund returning 7,98% (GBP) and 11,05% (USD) vs the MSCI ACWI which returned 6,92% (GBP) and 10,17% (USD). This indicates positive relative alpha generation, consistent with the Fund’s multi-manager strategy of selecting outperforming underlying managers.

Performance in April was broad-based, with particularly strong contributions from growth-oriented and emerging market exposures. Scottish Mortgage was the standout performer for April, benefiting from a rebound in global growth equities and producing a return of 18,39% and contributing 1,49% to the portfolio. T.Rowe Price Global Focused Growth Equity Fund delivered a strong return for the month of April at 13,66%, contributing strongly with 1,04% to the portfolio. The Templeton Emerging Markets Fund had a meaningful rebound in April, with a return of 10,89%, reflecting the meaningful recovery in emerging market equities from March. The Guinness Global Innovators, iShares MSCI World EUR Hedge and Jupiter Merian World Equity Fund also added meaningfully with return of 8,97%, 7,89% and 7,71% in April. The more value tilted strategies showed relatively muted gains with the Ranmore Global Equity Fund returning 3,21% and the Nomura Japan Strategic Value fund returning 2,45%.

In summary, April marked a strong recovery month, reversing March losses and restoring positive momentum. The Iza Global Equity Fund outperformed its benchmark, supported by effective manager selection. Growth-oriented and emerging market exposure were the primary performance drivers. Year to date the Iza Global Equity Funds returns remain solid but modest, reflecting earlier volatility. We continue to carefully model and monitor the positioning of the fund in the face of increasingly expensive, yet growth driven markets.

Quote of the month

You get recessions, you have stock market declines. If you don’t understand that’s going to happen, then you’re not ready.

Peter Lynch

Funds’ Performance Summary

Asset Class Performance (Base Currency)