Our report is available below

Click the image to view/download the PDF

Market Insights

June 2026 marked a turning point for financial markets as geopolitical tensions in the Middle East began to ease. A tentative agreement between the United States and Iran, including the reopening of the Strait of Hormuz, helped drive a sharp decline in oil prices and improved investor sentiment. Global markets responded positively, although volatility remained elevated and policymakers cautioned that inflation risks had not disappeared.

June 2026 marked a turning point for financial markets as geopolitical tensions in the Middle East began to ease. A tentative agreement between the United States and Iran, including the reopening of the Strait of Hormuz, helped drive a sharp decline in oil prices and improved investor sentiment. Global markets responded positively, although volatility remained elevated and policymakers cautioned that inflation risks had not disappeared.

Equity markets ended the second quarter strongly, supported by continued AI-related earnings growth and improving energy-market conditions. However, leadership became more selective as investors questioned stretched valuations in some technology sectors. June also brought the largest Initial Public Offering in history with the listing of SpaceX.

In South Africa, the focus remained on the consequences of the inflation shock that emerged during April and May. While economic growth showed resilience, higher fuel prices, elevated interest rates and global uncertainty continued to weigh on the outlook.

Global Markets – Equities: A Relief Rally Takes Hold

Global equity markets generally advanced during June as easing geopolitical tensions reduced fears of a prolonged global energy crisis. Key drivers of this included; progress toward a U.S.–Iran agreement, reopening of the Strait of Hormuz, falling oil prices, and continued strength in AI-related earnings and capital expenditure trends.

Major developed-market indices ended the second quarter with strong quarterly gains with the S&P500 up 14,38%, MSCI World up 11,65%, and the NASDAQ 100 up 26,76%, and investor confidence improved materially as the likelihood of severe energy supply disruptions diminished. However, performance was uneven underneath the surface. Technology and semiconductor stocks remained market leaders, while some previously high-flying AI names experienced increased volatility as investors became more selective.

Artificial intelligence continued to be the dominant investment theme globally. Positive factors included; strong semiconductor demand, ongoing corporate investment in AI infrastructure, productivity-enhancing technological adoption, and robust earnings growth from AI-linked companies. However, June also revealed signs of maturation within the AI trade with increased volatility in semiconductor shares, greater scrutiny of AI-related capital expenditure and wider divergence between winners and losers within the technology sector. The overall theme remains intact, but investors are increasingly focusing on profitability and execution rather than simply rewarding all AI-related businesses.

One of the most significant capital-market events of June was the successful initial public offering of SpaceX. The company priced its IPO at $135 per share, raising approximately $75 billion and valuing the business at roughly $1,77 trillion, making it the largest IPO in history. The listing was viewed as a major vote of confidence in long-term themes including space infrastructure, satellite communications, artificial intelligence, and advanced technology investment. Investor demand was exceptionally strong, reflecting continued appetite for companies positioned at the intersection of innovation and global technological transformation.

The IPO also reinforced the market’s preference for a relatively narrow group of large-scale growth companies. Similar to the AI-driven leadership seen throughout 2025 and 2026, SpaceX’s debut highlighted investors’ willingness to assign premium valuations to businesses with dominant market positions, strong competitive advantages and substantial long-term growth potential. However, the scale of the valuation also prompted renewed debate regarding concentration risk and whether investor expectations for future growth are becoming increasingly ambitious.

The biggest macroeconomic development during June was the sharp decline in oil prices due to the progress in Middle East peace negotiations. Brent crude fell toward the low-$70s range, WTI crude moved below $70 and energy market fears eased significantly. While this represented a major improvement compared to April and May, several factors remained unresolved namely shipping costs remained elevated, supply chains were still recovering, as well as some commodity prices remained above pre-crisis levels. Consequently, inflationary pressures were expected to fade gradually rather than disappear immediately. Gold prices declined notably as geopolitical concerns eased and expectations for tighter monetary policy strengthened.

Although oil prices fell, central banks remained cautious. At its June meeting, the Federal Reserve Kept rates unchanged, removed language suggesting a bias toward future rate cuts, signalled continued concern about inflation and highlighted strong economic activity and resilient labour markets. The June meeting was particularly important because it was the first chaired by Kevin Warsh, whose communication was interpreted as more hawkish than that of his predecessor. Markets increasingly shifted from expecting rate cuts to pricing in the possibility of additional tightening later in 2026, especially if inflation proves persistent.

Emerging Markets – Performance Moderates but Remains Constructive

Emerging markets generally benefited from improving global sentiment and lower oil prices, with supportive factors of reduced energy-related risks, improving investor risk appetite, continued technology-sector momentum and more stable trade conditions. However, market performance became increasingly differentiated with countries and companies linked to AI infrastructure and semiconductor production continued to outperform, while net energy importers and slower-growth regions remained more vulnerable. Despite improved sentiment, a number of headwinds are still present namely elevated global interest rates, persistent inflation pressures geopolitical uncertainty and dependence on technology-related growth themes.

South Africa

South African Markets – Economic Growth Remains Resilient

South Africa’s economy showed surprising resilience despite global volatility. According to the SARB Quarterly Bulletin, GDP grew by 0,5% during Q1 2026, marking this as the sixth consecutive quarter of expansion. Growth was supported by agriculture, mining and services sectors. The resilience of domestic activity helped offset concerns created by higher fuel prices and tighter financial conditions.

Inflation remained one of the dominant local themes with headline inflation printing at 4,0%, with fuel-related costs remained the primary driver of inflation. Transport and services inflation also contributed to upward pressure. While lower oil prices during June offered hope for eventual relief, policymakers remained concerned about second-round inflation effects.

The impact of the May rate hike continued to filter through the economy. With the repo rate at 7,0% and prime lending rate at 10,5%, the markets continued to assess the possibility of further tightening if inflation remained elevated. The SARB maintained a firm commitment to its inflation objective despite growing concerns regarding growth and household spending power.

The rand remained relatively resilient but volatile, influenced by the changes in Fed expectations, global risk sentiment and oil price developments. During the month the rand generally traded around the mid-R16/$ range, benefiting from improved sentiment while remaining vulnerable to shifts in global interest-rate expectations.

Special Themes and Policy Watch

Middle East Relief Changes the Narrative</h4

June represented the first month since the conflict began where investors focused on de-escalation rather than escalation.

The reopening of the Strait of Hormuz dramatically reduced fears of a prolonged energy shock and improved market confidence globally.

Inflation Has Peaked — But Has Not Disappeared

Falling oil prices improved the outlook, but inflation remained above target in many major economies. Central banks continue to worry that energy costs may have lasting effects resulting in wage pressures and services inflation remaining sticky.

The AI Theme Matures

The AI investment story remains powerful, but June demonstrated a shift toward greater selectivity. Markets are increasingly distinguishing between companies that are generating tangible earnings benefits and companies relying primarily on future growth expectations.

South Africa Shows Economic Resilience

Despite inflation and tighter policy settings, South Africa’s economy continued to expand. Growth in agriculture, mining and services helped offset some of the pressures created by higher interest rates, elevated fuel costs and global uncertainty.

Looking Ahead

Key issues likely to influence markets during July include:

- Sustainability of the U.S.–Iran agreement

- Whether lower oil prices translate into lower inflation

- Future Federal Reserve communication under Kevin Warsh

- SARB’s response to inflation developments

- Continued earnings momentum from AI-related industries

Closing Remarks

June 2026 marked a meaningful shift in market sentiment. The easing of Middle East tensions helped remove one of the largest risks facing investors, resulting in lower oil prices and improved confidence. However, the month also reinforced that the world economy remains in a transition phase. Inflation remains above target, central banks remain cautious, and market leadership is increasingly concentrated in a narrow set of high-growth themes. For investors, the environment continues to favour disciplined portfolio construction, diversification and a focus on quality businesses capable of navigating a more uncertain global landscape.

The Iza Portfolios

Iza Global Balanced Fund

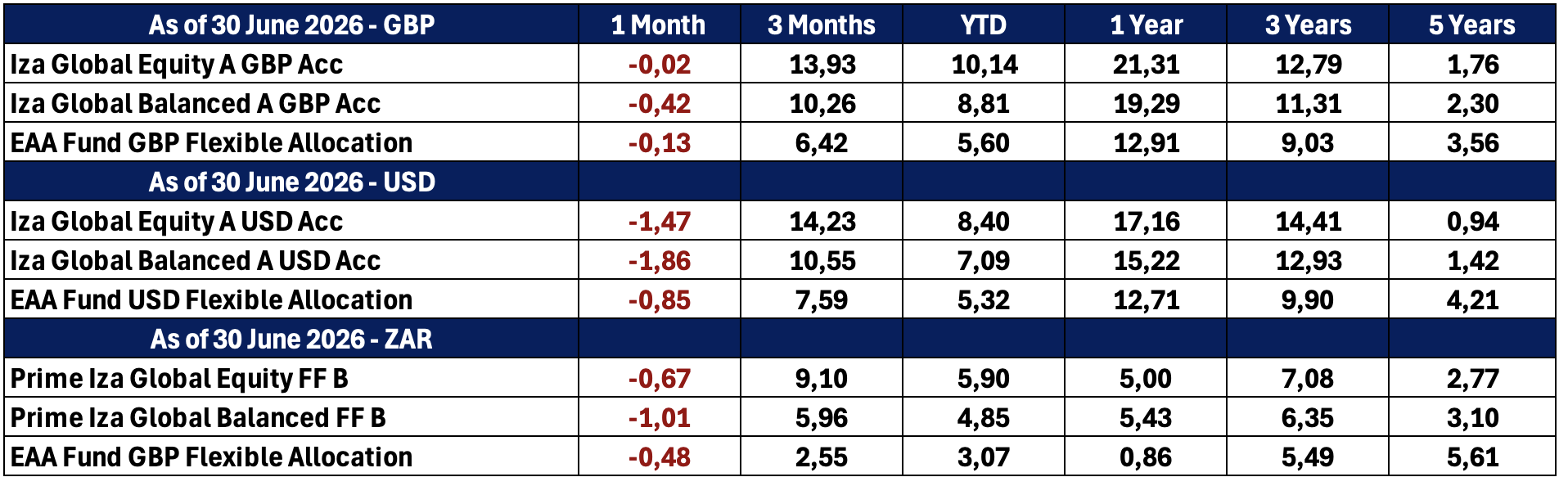

The Iza Global Balanced Fund delivered a return of -0,42% (GBP) and -1,86% (USD) during June, bringing its year-to-date return to 8,81% (GBP) and 7,09% (USD). Despite the modest decline during the month, the Fund continued to outperform its peer benchmark on a year-to-date basis (benchmark returns of 5,46% (GBP) and 4,92% (USD)) and maintained solid longer-term performance, with returns of 19,29% (GBP) and 15,23% (USD) over one year and 21,12% (GBP) and 27,04% (USD) over two years.

After two consecutive months of strong gains, June saw a more mixed market environment. While several underlying equity strategies continued to generate positive returns, weakness in growth-oriented holdings and alternative assets weighed on overall Fund performance. The strongest performing underlying holdings during the month were the Nikkei/Euro Stoxx 50/FTSE100 note delivering a positive return of 3,99%, the T-Rowe Price Global Focused Growth Equity Fund delivering a return of 1,57% and the Dodge and Cox Worldwide Global Stock Fund delivering a return of 1,33%. The main detractors during the month were gold with a negative return of -10,39%, reflecting a significant pullback in precious metals prices. Another large detractor to the portfolio was Scottish Mortgage which delivered a negative return of -3,38%, as growth-oriented equities experienced profit taking following strong gains in April and May.

In June our top contributions to performance were from the Dodge and Cox Worldwide Global Stock Fund, which contributed 0,16%. The T-Rowe Price Global Focused Growth Equity Fund once again forming part of our top contributors to performance contributing 0,13%.

In summary the Fund declined by -0,42% (GBP) and -1,86% (USD) in June, following strong gains in April and May. The primary driver for the decline in performance was due to the weakness in gold, commodities and growth-oriented equities. Positive returns from our allocation to global equity managers and structured products helped offset a portion of the negative returns. Despite the modest pullback, the Fund remains strongly positive for the year, with a year to date return of 8,81% (GBP) and 7,09% (USD), well ahead of its benchmarks at 5,46% (GBP) and 4,92% (USD). Overall, June represented a temporary pause in the Fund’s strong recovery trend, with diversified positioning helping to limit downside while preserving attractive year-to-date returns. The portfolio continues to maintain a balanced approach, combining growth opportunities with diversification through alternative investments, structured products, money market exposure and cash holdings.

Iza Global Equity Fund

The Iza Global Equity Fund delivered a relatively flat return of -0,02% (GBP) and -1,47% (USD) during June, following two exceptionally strong months in April and May. Despite the modest decline, the Fund maintained a robust year-to-date return of 10,14% (GBP) and 8,40% (USD), reflecting the strength of the recovery in global equity markets over the second quarter. The Fund slightly underperformed its benchmark, the MSCI ACWI Index, which returned 0,74% (GBP) and -0,80% (USD) during June. However, the Fund continues to deliver strong absolute returns and remains well-positioned over longer measurement periods, generating 21,31% (GBP) and 17,16% (USD) over one year and 22,85% (GBP) and 28,84% (USD) over two years.

June was characterized by a more mixed market environment. Equity markets paused after the strong gains recorded in April and May, with performance varying significantly across regions and investment styles. While several underlying managers continued to generate positive returns, weakness in higher-growth strategies weighed on overall Fund performance. The strongest-performing underlying holdings during the month included the Guinness Global Innovators Fund, delivering a return of 2,78%, the T-Rowe Price Global Focused Growth Equity Fund, delivering a return of 1,57%, and the Dodge and Cox Worldwide Global Stock Fund, delivering a return of 1,33%. The main detractor of the fund was Scottish Mortgage, which delivered a negative return of -3,38%, reflecting profit-taking in growth-oriented equities following significant gains in previous months.

In June our top contributions to performance were from the Dodge and Cox Worldwide Global Stock Fund, which contributed 0,17%. The Guinness Global Innovators Fund, which contributed 0,14%. The T-Rowe Price Global Focused Growth Equity Fund once again forming part of our top contributors to performance contributing 0,13%.

In summary the Fund recorded a marginal decline of -0,02% (GBP) and -1,47% (USD), effectively preserving capital in a more challenging market environment. Performance was held back primarily by weakness in growth-focused holdings, particularly Scottish Mortgage. Positive contributions from Dodge and Cox, T-Rowe and Guinness helped offset these losses. The Fund remains strongly positive for the year, with a Year to Date return of 10,14% (GBP) and 8,40% (USD), reflecting the benefits of its diversified multi-manager approach. Overall, June represented a consolidation month following strong second-quarter gains, with the Fund demonstrating resilience despite a softer market backdrop and remaining well-positioned for long-term capital growth.

Quote of the month

Investment success doesn’t come from buying good things, but from buying things well.

Howard Marks

Funds’ Performance Summary

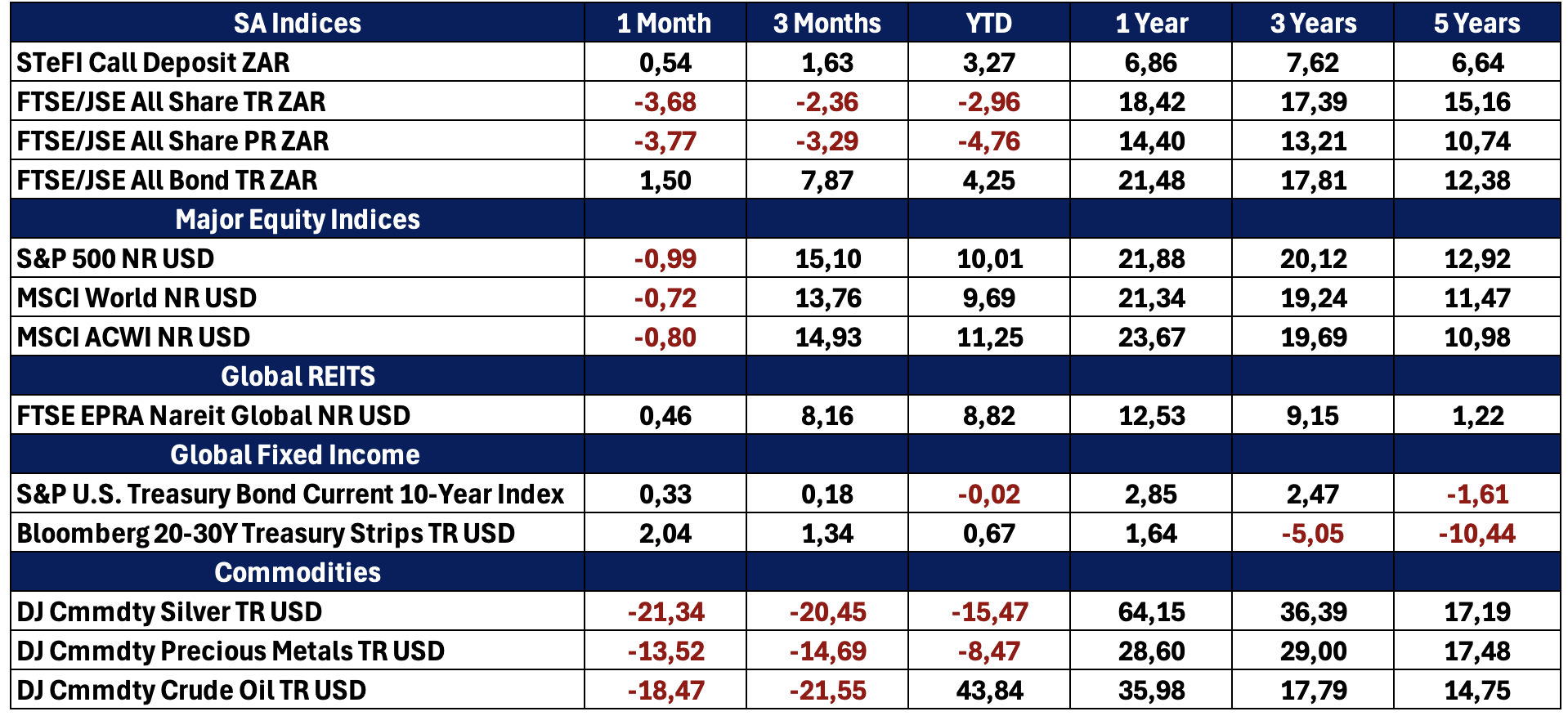

Asset Class Performance (Base Currency)