Our report is available below

Click the image to view/download the PDF

Market Insights

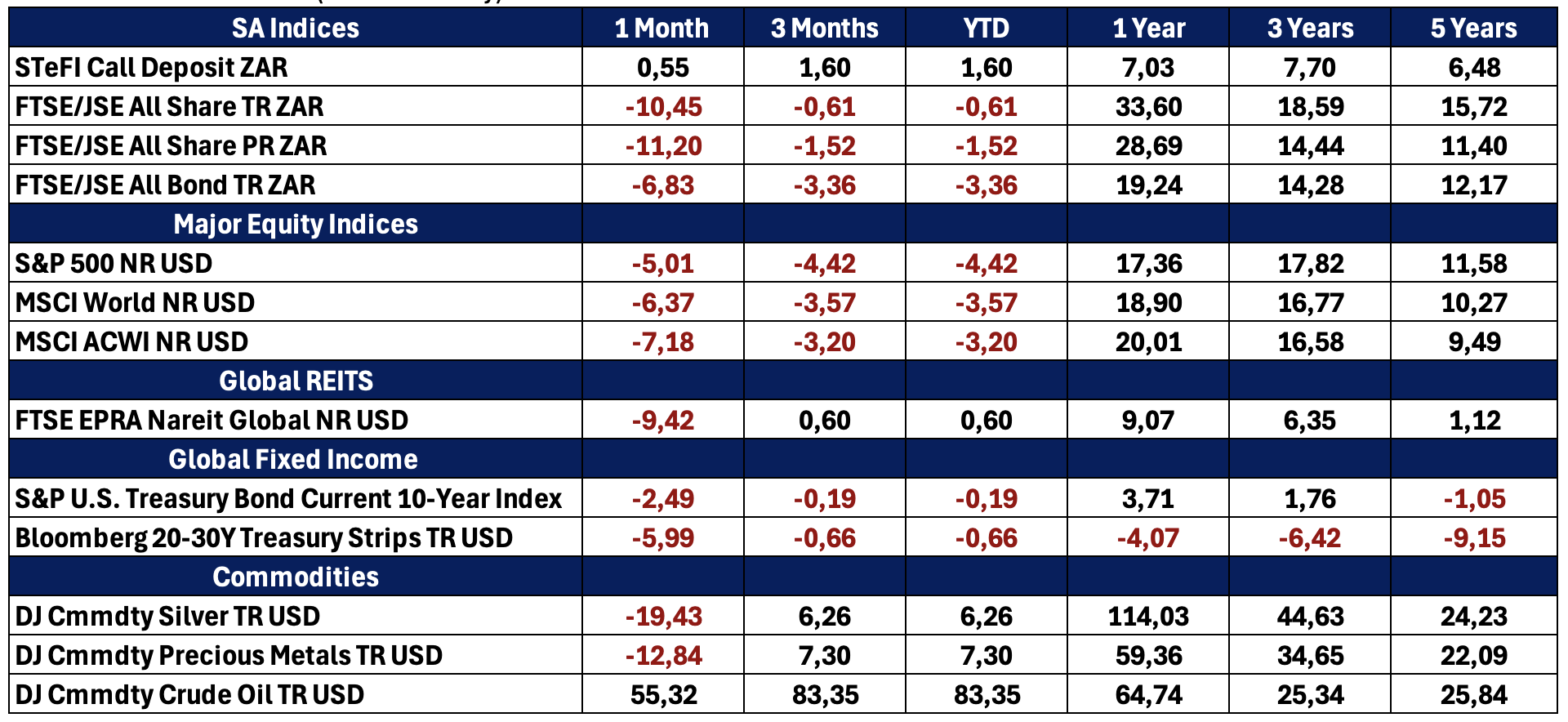

March 2026 marked a sharp inflection point for global markets, as geopolitical developments overwhelmed economic fundamentals. The escalation of the U.S.–Iran conflict and the effective closure of the Strait of Hormuz triggered one of the most severe energy‑supply shocks in decades, sending oil prices sharply higher and reigniting near‑term inflation concerns.

March 2026 marked a sharp inflection point for global markets, as geopolitical developments overwhelmed economic fundamentals. The escalation of the U.S.–Iran conflict and the effective closure of the Strait of Hormuz triggered one of the most severe energy‑supply shocks in decades, sending oil prices sharply higher and reigniting near‑term inflation concerns.

Equity markets declined meaningfully across most regions, bond yields moved higher, and risk appetite fell sharply. Emerging markets, which had entered the year strongly, experienced their steepest monthly setback in several years, while commodity exporters and energy producers were relative outperformers.

In South Africa, markets were volatile but comparatively resilient. The rand weakened early in the month amid higher oil prices, while the JSE fell sharply before stabilising toward month‑end. Inflation remained at target in February, but the South African Reserve Bank (SARB) adopted a more cautious tone, highlighting upside risks from global supply shocks while keeping rates unchanged.

Global Markets – A Broad Risk-Off Reset

Global equity markets fell sharply in March as geopolitical risk displaced economic resilience as the dominant driver of prices. Major indices recorded their worst monthly performance since 2022, with losses broad‑based across styles, sectors and regions. Even previously defensive diversification strategies offered limited protection as correlations rose sharply.

The S&P 500 experienced its worst month since September 2022, down -5,01% in Dollars, while European and Asian markets declined even more steeply, -9,80% and -13,23% respectively, due to their greater dependence on imported energy. Energy stocks were a notable exception, posting strong gains as oil prices surged.

The defining feature of March was the surge in oil prices. Brent crude recorded its largest monthly gain since the 1970s, driven by supply disruptions through the Strait of Hormuz, which handles roughly 20% of global oil flows. By late March, oil prices briefly exceeded $100 per barrel.

This energy shock reversed earlier disinflation progress and forced markets to reprice the outlook for interest rates and growth. In contrast, gold and silver, which had rallied earlier in the year, declined sharply as investors deleveraged and rising real yields reduced the appeal of non‑yielding safe havens.

Central banks globally responded with more hawkish and cautious messaging. The U.S. Federal Reserve held interest rates steady at 3,75% at its March meeting, citing elevated uncertainty around inflation, energy prices and geopolitical developments. While the Fed’s updated projections still indicate one rate cut later in 2026, markets significantly reduced expectations for near‑term easing.

Bond yields rose sharply during the month as investors reassessed inflation risks and policy trajectories, resulting in negative returns from both government and corporate bonds.

Emerging Markets – From Strong Start to Sharp Reversal

Emerging markets, which had been among the strongest performers earlier in 2026, endured a significant reversal in March. The MSCI Emerging Markets Index recorded its worst monthly decline since the pandemic, falling more than 13%, erasing year‑to‑date gains.

Energy‑importing countries were most affected, as higher oil prices worsened trade balances and inflation outlooks. Capital flows into emerging markets slowed abruptly, and EM bond issuance fell to its lowest March level since 2009.

Despite the broad sell‑off, dispersion across emerging markets remained notable. Energy exporters and select commodity‑linked economies fared better, while countries heavily exposed to energy imports or with external financing vulnerabilities were hit hardest. The month highlighted the importance of selectivity and diversification within EM allocations.

South Africa

South African Markets – Markets Navigate Global Shock

South African financial markets were swept up in the global risk‑off move but showed signs of resilience toward month‑end. The FTSE/JSE All Share Index fell sharply early in March, at one point trading about 10% below its February peak, before stabilising as commodity‑linked sectors provided support.

The rand weakened during the early part of the month, breaching R17,00 against the U.S. dollar as oil prices surged. As energy prices moderated slightly and global risk sentiment improved marginally, the currency recovered some ground by month‑end.

Encouragingly, South Africa entered this period of volatility with inflation firmly anchored. Headline and core inflation both printed at 3,0% for February, precisely in line with the SARB’s target.

At its March meeting, the SARB kept the repo rate unchanged at 6,75%, emphasising that the current shock is a classic supply shock. The Bank signalled it would look through first‑round price effects but remain vigilant against second‑round inflation risks. Its updated forecasts now see inflation peaking near 4% in the near term before gradually returning to target.

Special Themes and Policy Watch

Geopolitical Risk Dominates Market Behaviour

March underscored how quickly geopolitical developments can overpower macroeconomic fundamentals. The Middle East conflict not only affected energy markets but also disrupted shipping, insurance costs and global supply chains, increasing uncertainty for businesses and policymakers worldwide.

Inflation vs Growth: A Difficult Trade-Off

The energy‑driven inflation shock has placed central banks back into a challenging position: containing inflation expectations without unduly damaging growth. Markets repriced from expecting rate cuts to a “higher‑for‑longer” outlook, tightening financial conditions globally.

South Africa’s Relative Starting Position Matters

South Africa’s strong pre‑shock fundamentals, contained inflation, positive real rates and improving fiscal credibility, helped buffer the impact of global volatility. However, the country’s oil‑import dependence remains a key vulnerability during energy‑driven shocks.

Looking Ahead

As markets move into the second quarter of 2026, much will depend on:

- The duration and intensity of the Middle East conflict

- The trajectory of energy prices and inflation expectations

- Further signals from central banks regarding policy flexibility

- The resilience of emerging markets after March’s sharp correction

For South Africa, continued inflation discipline and credible policy responses will remain critical in navigating global uncertainty.

Closing Remarks

March 2026 was a reminder that geopolitical shocks can rapidly reshape market narratives. While long‑term fundamentals in many regions remain sound, short‑term volatility has increased meaningfully.

In this environment, diversified portfolios, disciplined rebalancing and a long‑term perspective remain essential. Periods of heightened uncertainty often create future opportunity, but patience and prudence are key.

The Iza Portfolios

IZA Global Balanced Fund

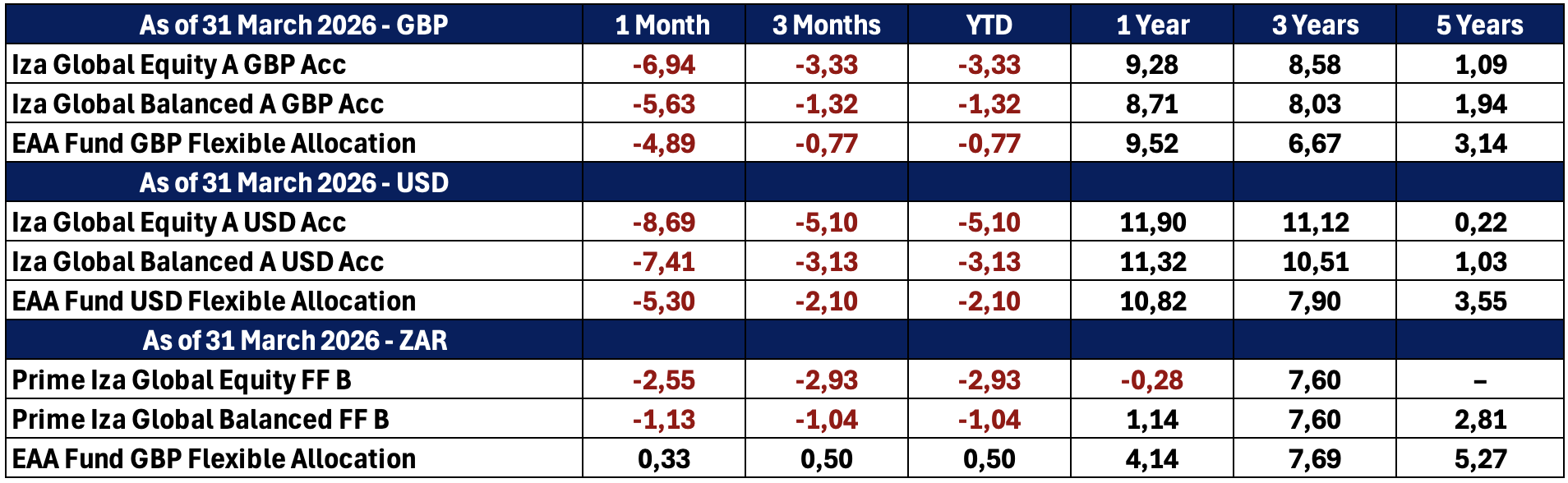

The Iza Global Balanced Fund concluded the month down by -5,63% in Pounds and -7,41% in Dollars, while the benchmark fell -4,90% in Pounds and -5,38% in Dollars. Year-to-date the fund was slightly negative by -1,31% in Pounds and -3,13% in Dollars compared to the benchmark which also declined -0,74% in Pounds and -2,06% in Dollars.

The month’s negative performance was attributed to the escalating Middle East conflict which prompted a sell-off of risk assets. Following the rising oil prices due to the conflict, we secured a 17,4% return on our oil note realised at the beginning of the month.

Emerging markets were particularly affected with the Templeton Emerging Markets Fund delivering a negative return of -9,32%, detracting from the portfolio by -0,51%. Despite the large risk-off event, the Nomura Japan Strategic Value Fund was one of the better-performing holdings within the portfolio for the month, only delivering a negative return of -1,32%, detracting from the portfolio by -0,06%.

We are confident that our current positioning and diversification will withstand the volatile headwinds ahead. With our consistent portfolio monitoring, we have the ability to swiftly adjust the portfolio to capitalise on potential opportunities presented by this pullback.

Iza Global Equity Fund

The Iza Global Equity Fund concluded the month down by -6,94% in Pounds and -8,69% in Dollars, while the MSCI ACWI fell -5,37% in Pounds and -7,18% in Dollars. Year-to-date the fund was down by -3,33% in Pounds and -5,11% in Dollars compared to the MSCI ACWI which also declined -1,96% in Pounds and -3,88% in Dollars. The month’s negative performance was attributed to the escalating Middle East conflict which prompted a sell-off of risk assets.

Emerging markets were particularly affected with the Templeton Emerging Markets Fund delivering a negative return of -11,03%, detracting from the portfolio by -0,92%. Despite the large risk-off event, the Nomura Japan Strategic Value Fund was one of the better-performing holdings within the portfolio for the month, only delivering a negative return of -1,32%, detracting from the portfolio by -0,07%.

The portfolio also experienced some meaningful performance detraction from funds such as the Guinness Global Equity Income Fund, Ishares MSCI World Euro Hedge and the Northstar Global Equity Fund. These detractions were -1,26%, -1,08% and -0,41% respectively.

While the portfolio ended the month with negative returns, we however are confident that our current positioning and diversification will withstand the volatile headwinds ahead. With our consistent portfolio monitoring, we have the ability to swiftly adjust the portfolio to capitalise on potential opportunities presented by this pullback.

Quote of the month

The big money is not in the buying or the selling, but in the waiting.

Charlie Munger

Funds’ Performance Summary

Asset Class Performance (Base Currency)