Our report is available below

Click the image to view/download the PDF

Market Insights

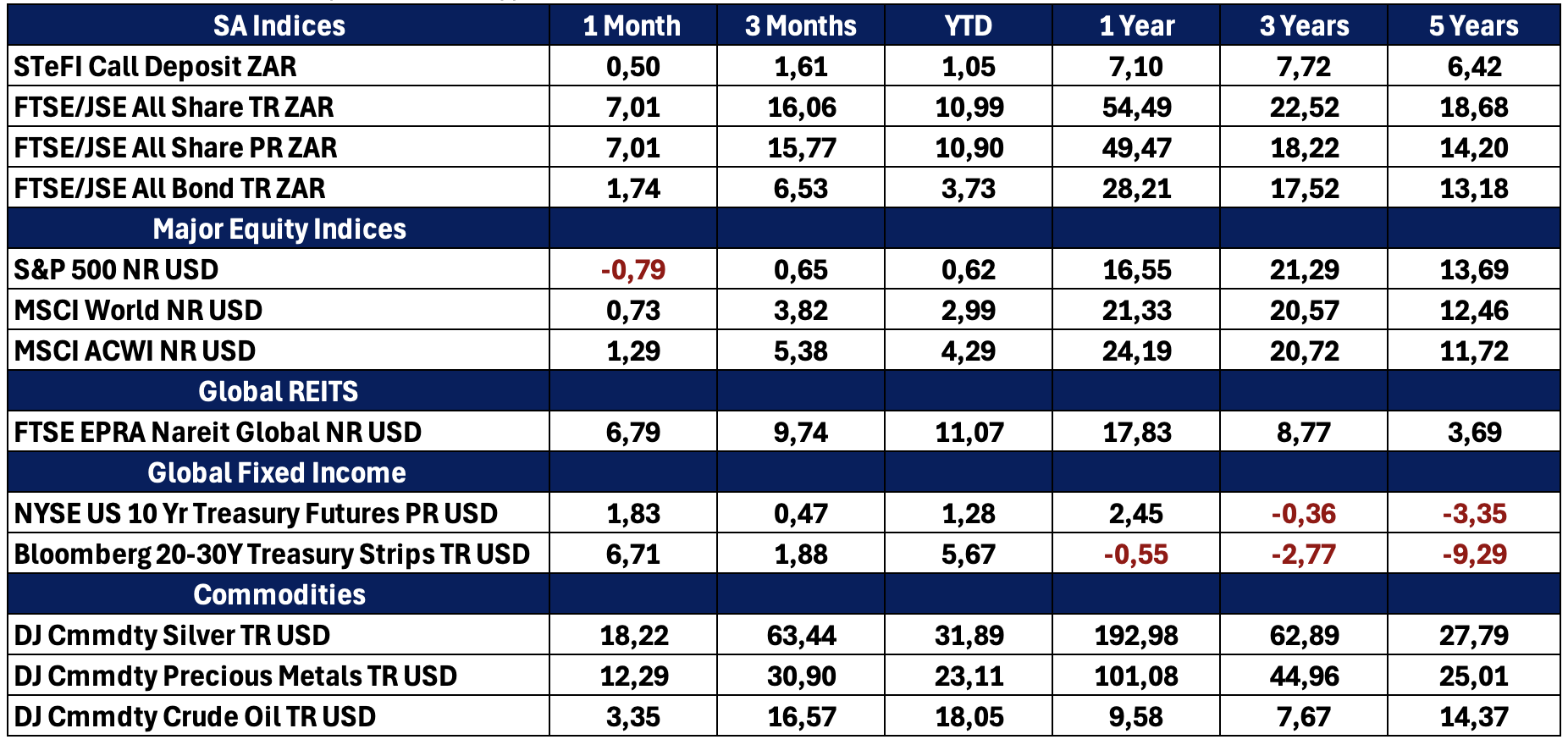

Global February 2026 delivered a complex and eventful month for global markets. Despite heightened geopolitical tensions; including U.S.–EU tariff brinkmanship over Greenland, escalating U.S.–Iran tensions, and ongoing instability in Venezuela; global markets remained generally resilient. Equity indices held firm, supported by stable economic data, strong early‑year earnings and continued momentum in AI‑related capital expenditure.

Global February 2026 delivered a complex and eventful month for global markets. Despite heightened geopolitical tensions; including U.S.–EU tariff brinkmanship over Greenland, escalating U.S.–Iran tensions, and ongoing instability in Venezuela; global markets remained generally resilient. Equity indices held firm, supported by stable economic data, strong early‑year earnings and continued momentum in AI‑related capital expenditure.

Emerging markets again outperformed developed peers, extending a powerful multi‑month rally driven by sustained capital inflows, a weaker U.S. dollar and ongoing strength in AI‑linked semiconductor demand.

In South Africa, February brought positive fiscal signals with the release of the National Budget 2026, which reinforced investor confidence through a credible debt stabilization path. The rand strengthened materially, bond yields declined and the JSE reached new all‑time highs. Inflation remained contained, with both CPI and PPI signalling a stable pricing environment.

Global Markets – Stability Amid Geopolitical Noise

Global equity markets were broadly stable in February, with the MSCI ACWI delivering a relatively flat return of 1,29% for the month. Despite headline risks; including tariff scares between the U.S. and EU over Greenland, civil unrest in Iran and political tensions in Venezuela; markets largely shrugged off the noise. Developed market equities performed steadily, supported by continued earnings growth and strong performance from semiconductor‑linked companies benefiting from AI investment cycles. Japan was a notable outperformer (MSCI Japan returned 9,90% in Yen) as snap elections delivered a supermajority supportive of fiscal stimulus.

February was marked by multi‑decade highs in gold and silver volatility. Gold’s volatility reached levels last seen during the 2008 financial crisis, while silver’s volatility matched early‑1980s highs. Rapid swings reflected speculative positioning, geopolitical risks and shifting sentiment toward safe‑haven assets. Oil prices also firmed amid escalating U.S.–Iran tensions, with Brent crude trending above $72 per barrel by mid‑month.

The U.S. Federal Reserve held its policy rate steady at 3.75% at the January meeting, and February commentary reinforced a data‑dependent stance. Core inflation remained “sticky,” with the core PCE index still near 2.8%, complicating expectations for cuts at the March meeting. Markets were divided, with some expecting easing by mid‑year and others pricing a prolonged pause.

New uncertainty was introduced with the nomination of Kevin Warsh as the next Federal Reserve Chair (a known inflation hawk) causing immediate reactions in equities, bonds and currencies.

Emerging Markets – A powerful and Broad-Based Rally Continues

Emerging Markets extended their exceptional start to 2026, outperforming developed peers for a third consecutive month. Performance was supported by a combination of U.S. dollar weakness, improving earnings trajectories and renewed investor appetite for regions leveraged to global manufacturing and AI‑related capex. North Asian exporters, particularly in South Korea, remained key beneficiaries.

While the rally was broad, differentiation remained important. Internal discussions and positioning reviews highlighted a preference for EM exposure with improving balance sheets, reform momentum and tangible earnings visibility, while frontier markets continued to face idiosyncratic fiscal and governance constraints.

South Africa

South African Markets – Budget 2026 Sparks a Strong Market Response

South Africa’s National Budget (25 February 2026) delivered a clear focus on fiscal consolidation, debt stabilization and structural reform, which markets welcomed. Treasury confirmed debt would peak at 78.9% of GDP in 2025/26, then gradually decline – a long‑awaited milestone. The announcement of a forthcoming legal fiscal anchor further boosted investor confidence.

Markets reacted swiftly with the Rand Strengthening significantly, closing near R15,85/$, the strongest level seen in months. Long-bond yields fell, reflecting the reduced risk premia and improved investor sentiment. The JSE reached new record highs, with the All-Share Index hitting 128,456 points and ending the month up 7,01%. The precious metal linked stock led the gains.

Inflation data continued to support South Africa’s credibility narrative with CPI for January printed at 3,5% year on year, reinforcing the SARB’s 3% inflation target, and producer price inflation eased to 2,2% year on year.

The Contained inflation allowed South Africa to maintain attractive real yields, key to ongoing rand strength and bond market performance.

Special Themes and Policy Watch

Geopolitics: Despite elevated global tensions — including U.S.–EU trade rhetoric, Middle‑East instability and political developments in Latin America — markets remained largely focused on fundamentals, with volatility concentrated in commodities and currencies rather than equities.

AI‑Driven Differentiation: The AI investment cycle continued to shape relative performance. Semiconductor manufacturers and enabling infrastructure outperformed, while select software names lagged amid disruption concerns. EM economies integrated into these supply chains saw amplified gains.

South Africa’s Fiscal Anchor: The February Budget’s proposed legal fiscal rule (expected later in 2026) could reshape long term market perceptions of South African fiscal sustainability. If implemented effectively, it may; reduce macro risk premia, support lower borrowing costs and strengthen sovereign‑credit narratives

February 2026 underscored a theme that has emerged over the past year: resilience.

Despite geopolitical shocks, tariff threats, commodity volatility and shifting monetary‑policy expectations, both global and domestic markets continued to adjust constructively. Emerging markets remained a standout, while South Africa delivered one of its most encouraging fiscal signals in years.

The Iza Portfolios

IZA Global Balanced Fund

The Iza Global Balanced Fund concluded February on a strong positive note. The fund achieved a positive return of 2.66% in Pounds and 1.12% in US Dollars, ahead of its peer benchmarks (2.14% in Pounds and 1.03% in US Dollars). February’s performance reflected effective diversification across equities, emerging market exposure and gold, alongside stabilizing contributions from fixed income as inflation pressures eased.

Key contributors included the Templeton Emerging Markets Fund, which produced a positive return of 7% (contributing 0,38%) for the month, benefitting from emerging market re‑rating momentum, and the Guinness Global Equity Income Fund, which continued to provide resilient returns with a lower‑volatility profile. Gold again proved an effective diversifier, provided an impressive return of 10.37% (contributing 0,45%) as inflationary and geopolitical uncertainties persist. Our portfolio positioning remained aligned with internal tactical discussions and Investment Committee guidance.

As we elaborated on last month, we are pleased to see that the tactical overweight to emerging markets has played out positively relatively quickly, albeit that we maintain our view that this positioning is longer-term focused looking at a minimum of 1-3 years out.

The Iza Global Balanced Fund is currently well positioned to capitalize on potential supply shocks to oil due to the ongoing conflict between the US and Iran through our oil note holdings.

The funds exposure to equities remains stable at 63,45% consistent with the prior month. This accounts for the prospective returns in each asset class and optimizes for an appropriate level of risk and return.

Iza Global Equity Fund

The Iza Global Equity Fund concluded the month with a positive return of 2.35% in Pounds and 0.82% in US Dollars, slightly trailing the MSCI All Country World Index which returned 3.38% in Pounds and 1.29% in US Dollars, and slightly lagging its peers benchmark of 2,99% in GBP and 0,90% in USD. Relative performance reflected positioning choices favouring valuation discipline and income resilience over momentum‑driven segments of the market.

Positive contributions came from Guinness Global Equity Income which continued to provide resilient returns with a lower‑volatility profile, Dodge & Cox Worldwide Global Stock and Jupiter Merian World Equity, while selective exposure to innovation‑oriented strategies provided measured participation in the AI theme.

Our tactical overweight towards emerging markets has continued to playout positively within a relatively short period of time, we however maintain our view that this positioning is longer-term focused looking at a minimum of 1-3 years out.

The Iza Global Equity Fund is well positioned and diversified to navigate the current macro and geopolitical uncertainty that we currently facing. Our portfolio positioning remains aligned with internal tactical discussions and Investment Committee guidance.

Quote of the month

You get recessions, you have stock market declines. If you don’t understand that’s going to happen, then you’re not ready.

Peter Lynch

Funds’ Performance Summary

Asset Class Performance (Base Currency)