Our report is available below

Click the image to view/download the PDF

Market Insights

Global markets entered 2026 on a more cautious but broadly constructive footing. January was characterized by heightened geopolitical and policy uncertainty, balanced against resilient economic data and improving inflation trends. While volatility increased at times, investor sentiment remained generally supportive of risk assets, particularly outside the United States.

Global markets entered 2026 on a more cautious but broadly constructive footing. January was characterized by heightened geopolitical and policy uncertainty, balanced against resilient economic data and improving inflation trends. While volatility increased at times, investor sentiment remained generally supportive of risk assets, particularly outside the United States.

Emerging markets stood out once again, extending the strong momentum seen in 2025 as capital flows continued to rotate toward non‑U.S. assets. In South Africa, markets benefited from a firmer rand, stable inflation and improved domestic fundamentals, even as the South African Reserve Bank (SARB) opted to pause its rate‑cutting cycle at its first meeting of the year.

Bond markets experienced some volatility during the month as investors adjusted expectations around the timing and pace of future rate cuts. Despite this, fixed income continued to attract interest as yields remained attractive relative to recent history.

The U.S. dollar weakened further in January, reflecting concerns around policy uncertainty and a growing shift toward global diversification.

Emerging Markets

Emerging markets were a key highlight in January, extending the strong rally that began in 2025. Equity markets across Asia and Latin America recorded robust gains, supported by favourable currency dynamics, capital inflows and improving growth expectations.

The primary drivers of EM strength included:

- Sustained U.S. dollar weakness, which supported EM currencies and reduced external financing pressures.

- Benign inflation trends, allowing many EM central banks to maintain or extend accommodative policy stances.

- Structural growth themes, particularly in technology, manufacturing and infrastructure.

Asian emerging markets continued to benefit from global investment in artificial‑intelligence infrastructure, while Latin American markets saw renewed interest following improved fiscal discipline and stabilizing macroeconomic conditions.

January saw strong inflows into emerging‑market equities, marking one of the strongest starts to the year for the asset class in over a decade. While some volatility emerged toward month‑end, overall sentiment remained firmly positive.

That said, performance dispersion across countries remained high, highlighting the importance of diversification and selective exposure within emerging markets.

South Africa

South African markets began the year on a firm footing, supported by a stronger rand, easing inflation and improving domestic confidence.

At its January meeting, the SARB kept the repo rate unchanged at 6.75%, following cumulative rate cuts in 2025. While inflation edged slightly higher in December to 3.6%, the SARB indicated that this was likely a temporary peak and reiterated confidence that inflation would trend lower over the course of 2026.

The decision to pause reflects the SARB’s cautious approach amid elevated global uncertainty, while still leaving the door open for further rate cuts later in the year should conditions allow.

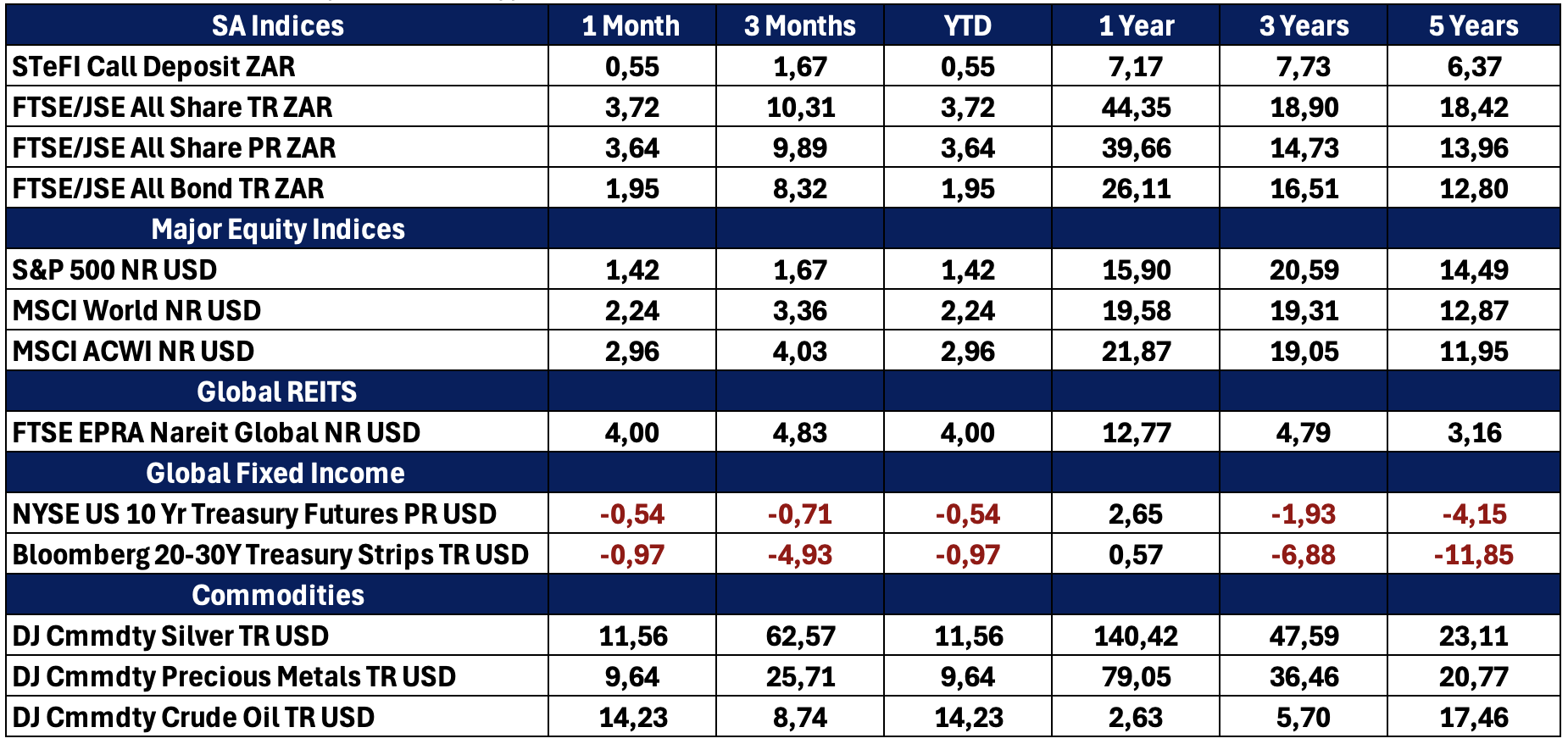

The FTSE/JSE All Share Index delivered solid gains in January, supported by strong performances in resource and financial stocks. Rising precious‑metal prices provided additional support to the local market.

South African bonds continued to perform well as inflation expectations remained anchored and real yields stayed attractive. The rand strengthened further, reaching its strongest levels since mid‑2022, benefiting from U.S. dollar weakness and increased investor confidence in South Africa’s macroeconomic trajectory.

January reinforced several important themes for investors:

- Markets remain sensitive to policy and geopolitical developments, even as economic fundamentals improve.

- Emerging markets continue to benefit from global diversification trends and supportive financial conditions.

- South Africa enters 2026 with improving macro stability, although structural challenges remain.

While short‑term volatility is likely to persist, the broader investment backdrop remains more supportive than in recent years. Maintaining diversified portfolios aligned with long‑term objectives remains key.

January 2026 set a measured but encouraging tone for the year ahead. With inflation largely under control, interest‑rate pressures easing and global growth proving resilient, investors remain positioned for opportunities — albeit with a heightened need for selectivity and discipline.

The Iza Portfolios

IZA Global Balanced Fund

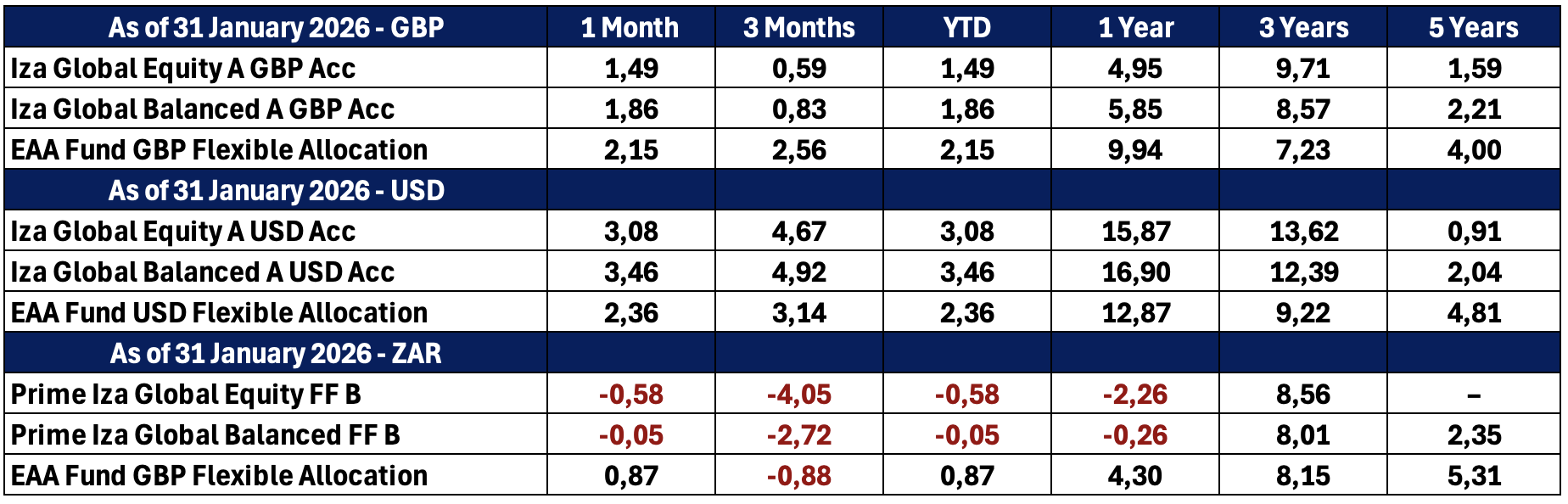

The Iza Global Balanced Fund closed the month of January up 1,86% (in Pounds) and 3,46% (in US Dollars). Our Strategic decision to broaden our emerging market exposure through the Templeton Emerging Markets Fund has paid off, with the fund achieving a positive return of 9,85% for the month. The Templeton Emerging Markets Fund was our largest contributor to performance for the month, contributing 0,50%. Gold performed excellent through the month of January by reaching a price of $5417,88 per ounce towards the end of January and subsequently falling to $4892,43 on January 30th. Despite this drop in price gold still managed to deliver an excellent return of 10,54%, contributing 0,43%. The rally in the gold price was driven by tight supply, increased retail and investment demand and geopolitical uncertainties, while the pullback was primarily caused by profit-taking, a pause in retail demand and inherent market volatility. January also saw WTI Crude Oil prices trend upwards due to concerns around supply, which provided a welcomed uptick in our WTI Crude Oil Note closing out at 9,02% for the month. The Guiness Global Equity Fund had a change in pace from December 2025 where is detracted from the portfolio to contributing 0,13% to the portfolio in January 2026, highlighting the volatility that is currently in the market. Scottish Mortgage continued its upward trend, providing a positive return of 5,86% for the month and contributing 0,46% towards the funds’ performance.

Iza Global Equity Fund

The Iza Global Equity Fund closed the month of January up 1,49% (in Pounds) and 3,08% (in US Dollars), outperforming the MSCI World index both in Pounds and US Dollars. Recent adjustments to the Iza Global Equity Fund included exiting the Prescient China Balanced Fund and reallocating to the Templeton Emerging Markets Fund to broaden and deepen emerging-market exposure with a more diversified approach, and exiting of the Nomura High Conviction Fund due to lagging performance and the introduction of the Jupiter Merian World Equity Fund and the Northstar Global Equity Fund to broaden our diversification through the use of an active systematic manager and a fundamental, bottom up approach that aims to consistently outperformance the benchmark.

Since the introduction of the Templeton Emerging Market Fund at the beginning of January, it has produced a positive return of 4,46% contributing 0,34% to the overall performance of the equity fund. Scottish Mortgage continued its upward trend, providing a positive return of 5,86% for the month and contributing 0,46% towards the funds’ performance, making Scottish Mortgage the biggest contributor to the overall performance of the fund in January. The Guiness Global Equity Fund had a change in pace from December 2025 where is detracted from the portfolio to contributing 0,19% to the portfolio in January 2026. Clearance Camino Continued into January with its positive performance, closing the month out with a positive return of 1,89%, contributing 0,14% to the overall performance.

Quote of the month

The single greatest edge an investor can have is a long‑term orientation.

Seth Klarman

Funds’ Performance Summary

Asset Class Performance (Base Currency)