Our report is available below

Click the image to view/download the PDF

Market Insights

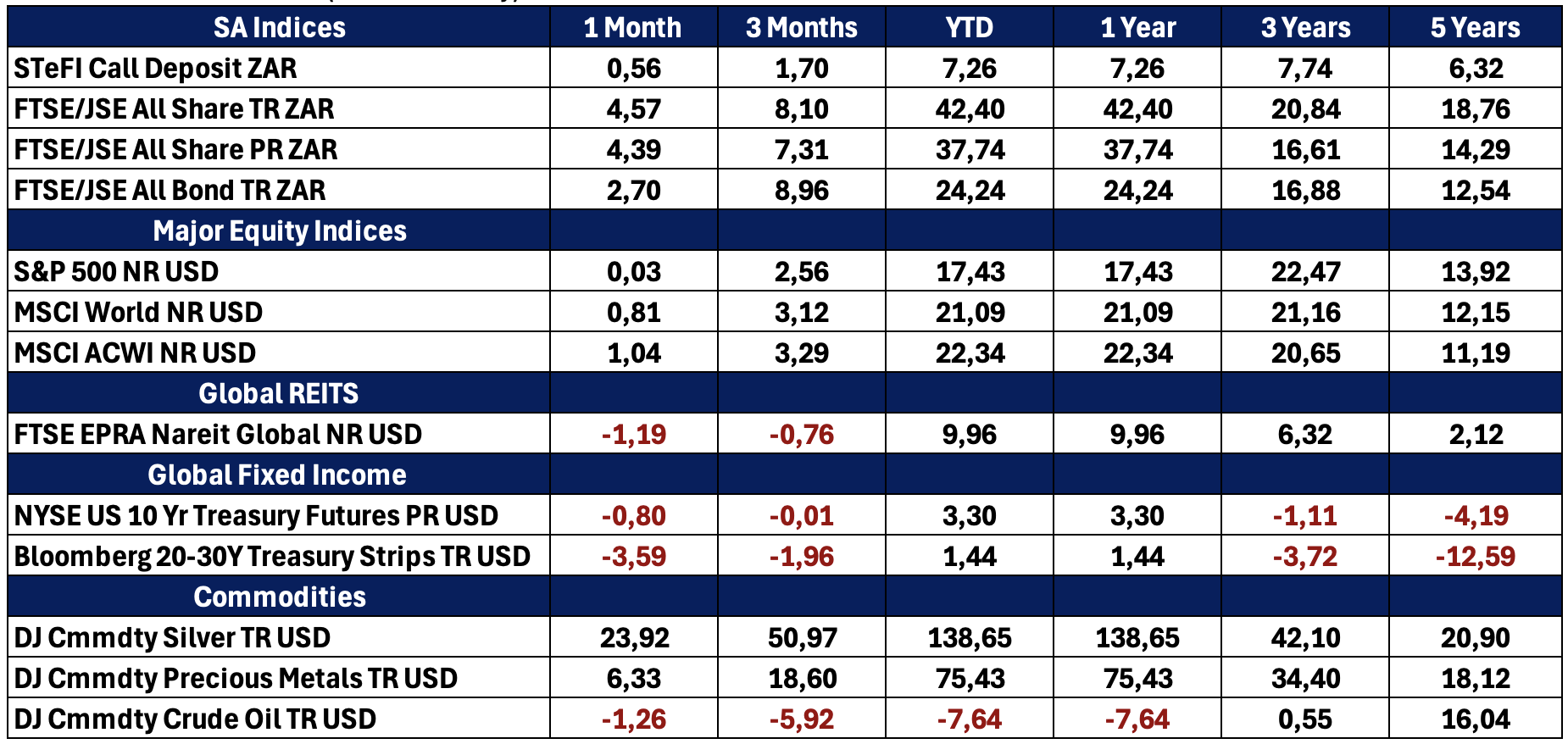

2025 proved to be a constructive year for investors, marked by easing inflation, improving financial conditions, and resilient corporate earnings. After several years of elevated volatility driven by global interest‑rate tightening and geopolitical uncertainty, markets responded positively as central banks began shifting toward more accommodative policy stances.

2025 proved to be a constructive year for investors, marked by easing inflation, improving financial conditions, and resilient corporate earnings. After several years of elevated volatility driven by global interest‑rate tightening and geopolitical uncertainty, markets responded positively as central banks began shifting toward more accommodative policy stances.

Global equities delivered strong returns, with performance broadening beyond the United States into Europe, Asia and emerging markets. Fixed income also staged a meaningful recovery as interest‑rate pressures eased. In South Africa, lower inflation, interest‑rate cuts and improved electricity supply provided welcome support to domestic assets and investor confidence.

Markets closed the year in December on a calmer and more consolidative note, setting a more stable platform for the start of 2026.

Global equity markets delivered a third consecutive year of positive returns in 2025, supported by moderating inflation and improving earnings growth. Importantly, market leadership widened meaningfully beyond the U.S., following a prolonged period of dominance by a small group of U.S. technology stocks.

European markets benefited from improving economic momentum and attractive valuations, while Asian markets were supported by strong demand linked to global investment in artificial intelligence and digital infrastructure. This broadening improved diversification benefits for investors with global exposure.

A key driver of market performance was the gradual shift in global monetary policy. After maintaining restrictive policy for much of the past two years, major central banks began easing financial conditions as inflation moved closer to target ranges.

In December, the U.S. Federal Reserve delivered its third interest‑rate cut of 2025, lowering its policy rate by 0.25%. While the decision was widely anticipated, the Fed signalled that further rate cuts are likely to proceed at a slower and more cautious pace in 2026, reflecting ongoing uncertainty around global growth and inflation trends.

Bond markets responded positively over the year as yields drifted lower, allowing both global and domestic fixed‑income assets to regain their role as stabilisers in diversified portfolios.

In currency markets, the U.S. dollar weakened further in December, ending the year significantly lower against most major and emerging‑market currencies. This supported international equity returns and helped improve financial conditions in several emerging markets.

Emerging Markets

Emerging markets were among the best‑performing asset classes of 2025, marking a notable turnaround after several years of pressure from high global interest rates and currency volatility.

Emerging market equities delivered strong double‑digit returns, outperforming developed markets in aggregate. The MSCI Emerging Markets Index rose by more than 30% in USD terms over the year, with performance broad‑based across Asia, parts of Latin America, and select Eastern European markets.

Three key factors drove this improvement:

- A weaker U.S. dollar, which supported EM currencies and capital flows.

- Earlier interest‑rate cuts by several emerging‑market central banks as inflation eased.

- Structural growth themes, particularly in Asia, linked to technology, manufacturing and infrastructure investment.

Emerging markets ended the year on a firm but more measured note, as investors locked in gains and reduced risk toward year‑end. Despite some profit‑taking, overall sentiment toward the asset class remained positive, supported by stable currencies and improved global liquidity conditions.

Looking ahead, emerging markets appear better positioned than in recent years, although performance is likely to remain uneven across regions, reinforcing the importance of diversification and careful selection.

South Africa

South African assets benefited from a meaningfully improved economic environment in 2025. Inflation declined steadily through the year, remaining comfortably within the South African Reserve Bank’s (SARB) target range.

In response, the SARB reduced interest rates in the second half of the year, with the repo rate ending 2025 at 6.75%. This provided relief to consumers and businesses and improved the outlook for local economic activity.

A major positive development was the marked improvement in electricity supply reliability. Sustained progress at Eskom led to long periods without load shedding, supporting business confidence and reducing a key constraint on economic growth.

The FTSE/JSE All Share Index delivered strong gains in 2025 and closing near record highs. Gains were supported by resource stocks, financials and improved risk appetite toward domestic assets.

South African bonds also performed well as inflation moderated and interest rates declined. The rand strengthened significantly, benefiting from a softer U.S. dollar, attractive real yields, and improving investor confidence in South Africa’s macroeconomic stability.

In December, local markets consolidated gains following a strong year. Trading activity slowed, in line with typical year‑end patterns, but sentiment remained constructive. The improved electricity outlook, stable inflation, and supportive monetary policy helped reinforce confidence going into 2026.

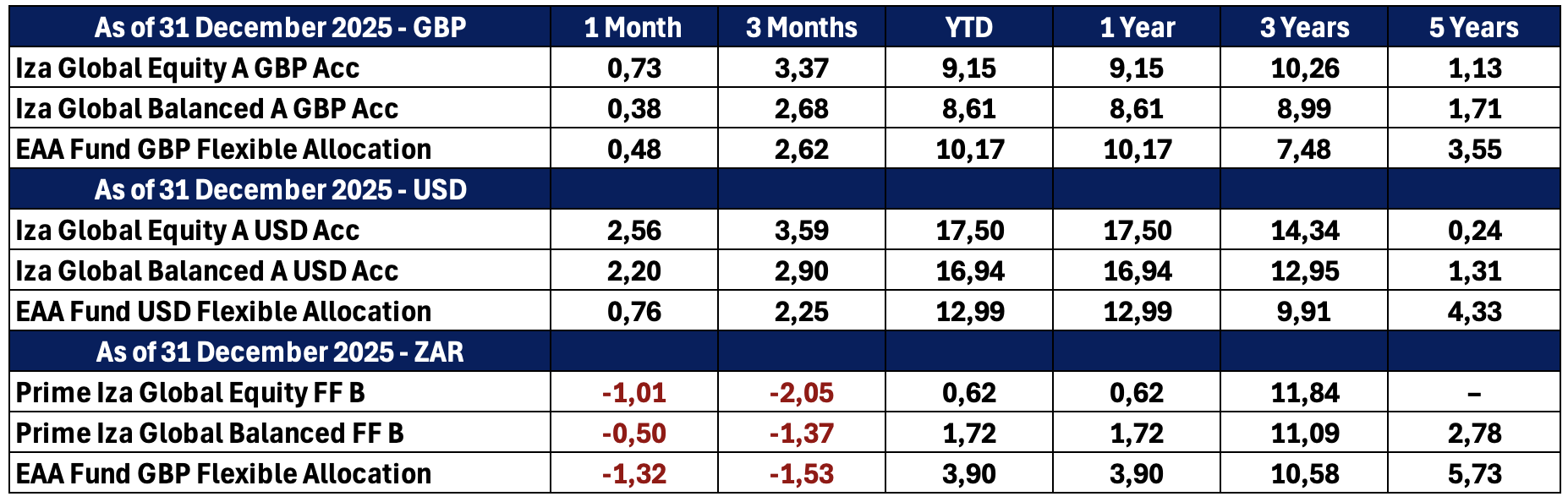

The Iza Portfolios

IZA Global Balanced Fund

The Iza Global Balanced Fund experienced a rebound in December from November, closing the month at 0.38% up in Pounds and 2.20% up in Dollars. Our strategic decision to diversify our MSCI holdings across different currencies has enabled us to profit from the weakening dollar against the pound. Scottish Mortgage was the largest contributor to the fund during December, contributing 79 bpts. Scottish Mortgage’s December performance was largely due to specific developments regarding SpaceX’s impending IPO. Gold was relatively flat for the month of December but over the last year it has produced a return of approximately 64.37% in US Dollars, placing it as one of the fund’s top contributors. The Guinness Global Equity Income Fund detracted from the fund in December by 13 bpts. However, the fund’s value and dividend-focused approach which offers long-term sustainability remains vital to the portfolio.

Reviewing the 2025 year, our decision to allocate a portion of the portfolio to the MSCI World has been successful, contributing a positive return of 2.15% (in Pounds). The Iza Global Balanced Fund achieved a positive return of 8.61% (in Pounds) for the year, just below the GBP benchmark, and 16.94% (in US Dollars) outperforming the US Dollar Benchmark. Key underlying contributors included strong performance from Dodge & Cox (15.84% GBP terms, contributing 1.78%), Scottish Mortgage (24.72%, contributing 1.50%), and TROWE (13.38%, contributing 0.88%). Gold added meaningful value (1.46% contribution), providing diversification during periods of equity weakness. Guinness Global Equity lagged (3.72%) amid quality-focused headwinds.

Recent portfolio adjustments included exiting the Prescient China Balanced Fund and reallocating to the Templeton Emerging Markets Fund to broaden and deepen emerging-market exposure with a more diversified, value-oriented approach.

Looking ahead to 2026, we remain cautiously constructive on risk assets but expect continued volatility driven by geopolitical tensions and policy uncertainty. The IZA Segregated Mandate continues to offer an attractive yield of approximately 4%, slightly above the Bloomberg Global Bond Aggregate, delivering a decent real yield in the current environment. Recent escalations in US military engagement and the incoming Trump administration’s pressure on the Federal Reserve raise risks of higher inflation, looser fiscal policy, and potential dollar depreciation. These factors reinforce our decision to maintain meaningful exposure to Gold as a hedge against currency debasement and geopolitical risk.

Iza Global Equity Fund

The The Iza Global Equity Fund experienced a rebound in December from November, outperforming the MSCI World Index in both Pounds and US Dollars. The Fund achieved a return of 0.73% in Pounds and 2.56% in US Dollars. Clearance Camino closed the month with a return of 1.43% in Pounds as the European property markets ended 2025 on a firmer footing. December confirmed stabilising valuations and a gradual recovery in investment activity. Transaction volumes increased into year-end, supported by easing financing conditions and renewed institutional participation. Scottish Mortgage was the largest contributor to the fund during December, contributing 85 bpts. Scottish Mortgage’s December performance was largely due to specific developments regarding SpaceX’s impending IPO.

The Iza Global Equity Fund closed the year with a positive return of 9.14% (in Pounds) and 17.51% (in US Dollars) underperforming its MSCI World benchmark. The portfolio navigated a challenging environment but lagged due to style headwinds in quality/growth segments and muted returns from certain core holdings. Standout underlying performers included Scottish Mortgage Trust at 24.72% (contributing 1.88%), Dodge & Cox Stock Fund at 15.84% (2.16% contribution), and T. Rowe Price at 13.38% (0.94% contribution). Guinness Global Innovators (12.10%) and Clearance (11.83%) added value, while Guinness Global Equity (3.72%) and Nomura USD (-0.23% contribution) were notable laggards.

Looking ahead to 2026, we maintain a constructive but selective stance on global equities, with increased emphasis on emerging markets. Escalations in US military engagement and the incoming Trump administration’s pressure on the Federal Reserve heighten risks of inflationary policies, fiscal expansion, and potential dollar weakness. These dynamics support our consideration in favour of emerging markets where valuations remain attractive relative to developed markets.

Quote of the month

The big money is not in the buying or the selling, but in the waiting.

Charlie Munger

Funds’ Performance Summary

Asset Class Performance (Base Currency)