Our report is available below

Click the image to view/download the PDF

Market Insights

September 2025 turned out to be a notably positive month for global equity markets. The S&P 500 rose approximately 3.6%, buoyed by strong gains in mega-cap growth stocks centered in the technology and communication sectors. The rally was largely driven by the Magnificent 7 which outperformed and powered much of the upside in the benchmark. Meanwhile, the Russell 2000 small-cap index advanced about 3.1%, slightly underperforming the S&P 500 but still reflecting a moderate appetite for risk among investors. The small-cap market also achieved a new all-time high for the first time since 2021, signaling breadth to the rally beyond just mega-caps.

September 2025 turned out to be a notably positive month for global equity markets. The S&P 500 rose approximately 3.6%, buoyed by strong gains in mega-cap growth stocks centered in the technology and communication sectors. The rally was largely driven by the Magnificent 7 which outperformed and powered much of the upside in the benchmark. Meanwhile, the Russell 2000 small-cap index advanced about 3.1%, slightly underperforming the S&P 500 but still reflecting a moderate appetite for risk among investors. The small-cap market also achieved a new all-time high for the first time since 2021, signaling breadth to the rally beyond just mega-caps.

China’s equity market surged dramatically, with the MSCI China Index gaining around 9.8%. This outperformance was fuelled by government measures to stabilize industrial profits alongside easing trade tensions, creating a risk-on environment amid some domestic economic challenges. Emerging markets broadly echoed this positive tone, with the MSCI Emerging Markets Index climbing 7.2%, supported by currency strength, upbeat earnings reports, and optimism around AI-related growth prospects. EM currencies strengthened, enhancing returns, with countries like South Korea and South Africa benefiting.

Growth stocks outperformed value stocks, while technology and communication sectors led, and energy, consumer staples, and materials lagged. The technology and innovation sectors within growth stocks keep attracting investors thanks to advances in AI, cloud computing, and digital transformation, making these companies look more appealing for long-term growth despite higher valuations. Value stocks have underperformed as they face challenges from inflation and slower economic growth. Investor sentiment also favours growth stocks, driven by optimism about future earnings and disruptive technologies, despite their elevated price premiums. This momentum is expected to continue until significant changes in monetary policy or economic outlook shift the risk appetite.

The UK market experienced challenges with inflation of 3.8% prompting static rates from the Bank of England. Borrowing costs hit a 27-year high, manufacturing remained in contraction (PMI 47), but the service sector showed strength with a 16-month high PMI of 54.2. The widened trade deficit reflected impact from trade tensions. The UK’s FTSE 100 lagged behind, impacted by persistent inflationary pressures, weaker manufacturing activity, and cautious investor sentiment, resulting in flat to slightly negative returns for the month.

The bond market delivered positive performance supported by a mix of macroeconomic developments and central bank actions. U.S. government bonds rallied as weaker-than-expected employment data and dovish commentary from the Federal Reserve raised expectations for further rate cuts before year-end. The 2-year U.S. Treasury yield edged down slightly, while the 10-year yield fell by about 8 basis points, supporting gains in both government and investment-grade corporate bonds.

In the UK, government bonds (gilts) experienced volatility but ultimately ended the month in positive territory despite persistent inflation and higher borrowing costs. Corporate bonds and emerging market debt also delivered solid returns, buoyed by positive investor sentiment and improving credit fundamentals. High-yield bonds benefited from a risk-on environment, while inflation-linked bonds provided some cushion amid sticky inflation pressures.

South Africa

Global risk assets advanced through September, buoyed by steady economic momentum and the US Federal Reserve’s decision to ease policy again. While developed-market equities look expensive by traditional measures, liquidity and confidence in the soft-landing narrative helped extend gains. Emerging-market peers benefited disproportionately from renewed capital inflows, a weaker dollar, and firm commodity markets.

South African equities delivered their strongest performance in almost two years, climbing 6.6% over the month. The standout driver was the Resources sector, which surged 28.1% — its best monthly return in nearly two decades and more than doubling in value since the start of the year. Industrials eked out a gain of 1.7%, but most other sectors underperformed, with Chemicals (-8.9%) and Life Insurance (-7.9%) notable laggards. The bond market also impressed, with a 3.3% return, marking its best month since September 2024. Investors extended duration as yields compressed to multi-year lows, encouraged by strong foreign demand (net inflows of R7.7bn) and a constructive inflation backdrop. Inflation-linked bonds also firmed, although liquidity frictions made the move less uniform than in nominals. Local property retreated 1.0%, weighed down by offshore-focused counters, but Q3 still closed +5.5% higher, taking year-to-date returns to almost 12%.

The SARB’s Monetary Policy Committee opted to leave the repo rate unchanged at 7.0%, though the decision was finely balanced with two members favouring another cut. Policymakers reiterated their intention to anchor inflation closer to 3%, even if that requires a restrictive stance in the short term. Encouragingly, headline CPI slowed to 3.3% in August (from 3.5% in July), defying forecasts for a rise, thanks largely to softer food and fuel prices. Core inflation nudged up to 3.1%, consistent with expectations. The SARB upgraded its near-term inflation forecast slightly but with inflation outcomes surprising to the downside and the rand trading stronger, the door remains open for easing later this year.

On the growth side, momentum improved. Q2 GDP expanded by 0.8% q/q, the best performance in two years and above consensus. Mining (+3.7%), manufacturing (+1.8%), and trade (+1.7%) all contributed positively, while household consumption rose 0.8% on the back of rising real incomes and prior rate cuts. Investment activity remained a weak link: gross fixed capital formation contracted 1.4%, reflecting continued retrenchment by state-owned firms, though private sector investment turned modestly positive. A key concern is nominal GDP, which slowed to 2.5% y/y, well short of Treasury’s 5.8% assumption and implying potential shortfalls in revenue collection.

The global backdrop is broadly supportive. Record highs in gold and renewed strength in platinum prices boosted South Africa’s export earnings and fiscal buffers. A softer dollar following Fed easing lifted the rand to below R17.40/$, improving sentiment and lowering imported inflation risks. However, several risks linger: the expiry of AGOA and slow progress on securing a new US trade deal weigh on the trade outlook; Washington’s widening tariff programme raises uncertainty; and geopolitical flashpoints — from Russia-Ukraine to the Middle East — continue to stir volatility in global energy markets.

In sum, September delivered a strong run for South African financial markets, underpinned by global liquidity, favourable commodity dynamics, and a better-than-expected domestic inflation and growth profile. Yet, persistent weakness in investment, concerns over fiscal sustainability, and unresolved trade negotiations temper the outlook, underscoring the need for structural reform to sustain momentum.

The Iza Portfolios

IZA Global Balanced Fund

The IZA Global Balanced Fund has outperformed both the USD and GBP benchmarks in absolute terms in September. Our balanced exposure to both pounds and US dollars acted as a significant diversifier to the portfolio returns. With the US dollar weakening amid geopolitical uncertainties and shifting monetary policies, the equal exposure to GBP and USD smoothens the portfolio volatility making the portfolio more resilient to currency shocks.

The top contributors to the fund performance were mostly from the growth themes. The MSCI World Index benefited from broad gains across global equity markets, led by technology and growth sectors that continued to outperform. Growth themes such as artificial intelligence and cloud computing fuelled investor enthusiasm, while resilient consumer spending and positive earnings reports provided underlying support. The current market environment favoured innovation-driven growth stocks, while benefiting from a global economic backdrop of robust consumption and technological advancement.

Scottish Mortgage (SMT LN) continued to deliver strong returns due to its concentrated exposure to technology leaders and emerging growth disruptors as these themes gained traction, aligning well with positive market sentiment towards long-term transformative trends. SMT LN continues to be a significant uplift to the returns given the strong demand for high growth innovative companies.

September 2025 proved to be a standout month for SPDR Gold Shares ETF (GLD) – up about 12% in GBP, reflecting surging gold prices and robust investor demand amidst a backdrop of economic uncertainty. Gold hit multiple all-time highs during the month, fuelled by concerns about inflation, geopolitical tensions, and risks surrounding the U.S. government, including a looming shutdown.

The bond holdings delivered slightly positive returns benefiting from stable economic conditions and declining Treasury yields. U.S. high-yield bonds and emerging market debt delivered modest positive returns, supported by renewed investor demand, robust refinancing activity, and a favourable credit environment, contributing to overall resilience in the enhanced yield bond space.

Iza Global Equity Fund

The IZA Global Equity Fund delivered strong positive returns while slightly lagging both benchmarks. We believe that our portfolio holds positions in high-quality companies well positioned to mark-up with market expectations over time. While some volatility is expected following recent strong price advances, the outlook for many key sectors of the global economy remains compelling.

Our recent addition, Ranmore Global Investor added significant upside to the portfolio performance since addition benefiting from its value-oriented strategy and reduced exposure to Western markets in favor of Asia, particularly South Korea and Japan, where dividend yields remained attractive. The fund’s consistent ability to navigate market cycles and deliver positive gains has sustained strong investor interest and inflows throughout 2025.

The Guinness Global Innovators Fund performed strongly in September 2025, driven by its focus on technology, software, and healthcare sectors where innovative companies delivered solid earnings and growth. Year-to-date, the fund has continued to outperform, benefiting from its exposure to market leaders in AI, cloud computing, and digital transformation, making it a favorite for investors seeking high-quality, innovation-led growth. This thematic focus on companies with sustainable competitive advantages has helped the fund navigate market volatility and deliver consistent returns.

The property fund, Clearance Camino has been a laggard this month which detracted the returns. In the UK, while house prices rose modestly, the broader property market faced challenges from political uncertainties and regulatory speculation, leading to cautious buyer sentiment. Across Europe, economic uncertainties and geopolitical tensions dampened investor confidence, contributing to subdued activity and price pressures in some regions. Despite these headwinds, pockets of resilience emerged in sectors like offices and residential lettings, reflecting ongoing demand amid constrained new construction and shifting market dynamics.

China has been a great contributor to delivering strong positive returns in September 2025, driven by several factors despite ongoing economic challenges. Retail investor enthusiasm also played a major role, as many shifted monies from bank deposits to equities amid disappointing property market conditions and declining deposit rates. Key technology and new energy stocks led gains, and the Shanghai Composite reached its highest level in over a decade. This rally reflected optimism about China’s transition toward innovation-led growth and supportive policy measures, even as some economic indicators signaled a slowdown.

Overall, we still believe that the portfolio positioning and strategy are in line with our expectations.

Key Performance Highlights across both funds

Contributors across both funds:

T.Rowe (MTD: 4.91% and YTD: 7.66%) The T. Rowe Price Global Equity Fund performed positively in September 2025, supported by strong contributions from growth-oriented sectors like technology and healthcare, which benefited from sustained innovation and earnings momentum. Year-to-date, the fund has delivered solid returns above many benchmarks, driven by its focus on high-quality companies with durable growth prospects and a diversified global portfolio that has helped navigate market volatility effectively.

Prescient China (MTD: 4.78% and YTD: 10.99%) The Prescient China Balanced Fund delivered strong returns in September 2025, buoyed by strong equity gains particularly in key sectors like financials and technology, combined with effective risk management through balanced fixed income exposure. This blend helped capture upside in a recovering Chinese market while mitigating volatility, contributing to its strong monthly return.

Dodge & Cox Global Stock Fund (MTD: 2.13% and YTD: 11.33%) Dodge & Cox Worldwide Stock Fund continued to deliver consistent returns in GBP this month due to its disciplined value investing approach, focusing on high-quality, undervalued companies with strong cash flow and resilient business models.

Ishares Core MSCI World The MSCI world ETF continues to add significant upside to the portfolio with a MTD with over 3% in GBP. The fund benefits from its diversified portfolio of high-quality, large-cap stocks in sectors like technology, healthcare, and consumer discretionary, which have shown resilient earnings growth and innovation-driven momentum throughout 2025.

Quote of the month

Be fearful when others are greedy and greedy when others are fearful.

Warren Buffett

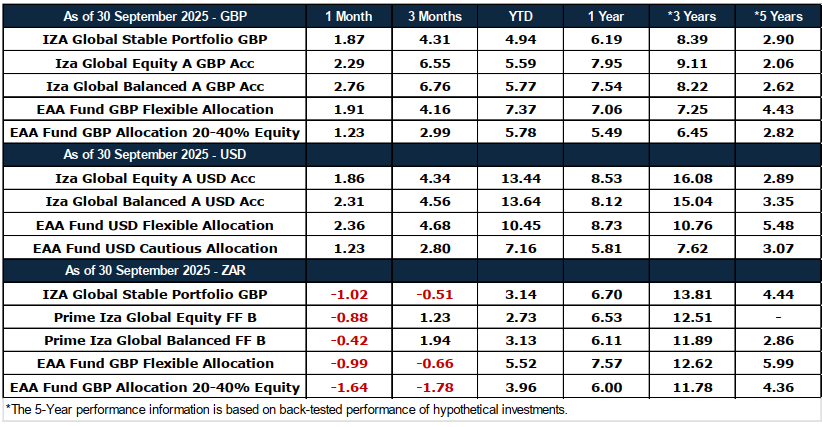

Funds’ Performance Summary

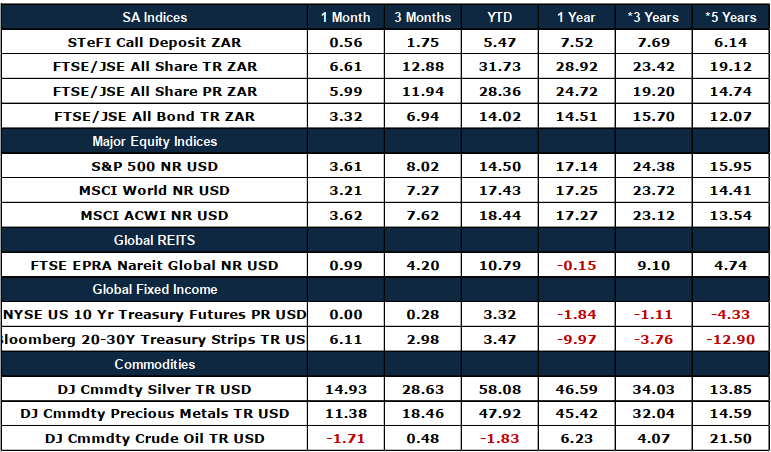

Asset Class Performance (Base Currency)