Our report is available below

Click the image to view/download the PDF

Market Insights

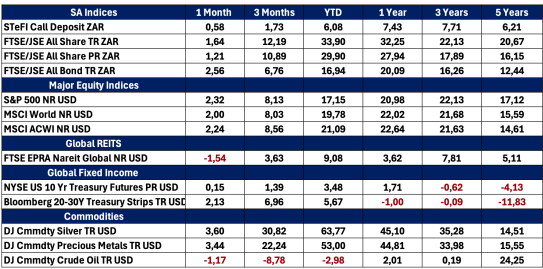

October 2025 delivered moderate gains across global equity markets. The S&P 500 rose 2.27%, led by mega-cap technology stocks benefiting from strong earnings and AI-driven growth. The Russell 2000 returned 1.76%, continuing its upward trend but underperforming large caps. China’s equity market declined, with the MSCI China Index falling 3.81% due to concerns over export controls and domestic economic softness. Emerging markets gained 3.8%, supported by strong tech performance in South Korea and Taiwan, currency strength, and optimism around industrial AI growth. Growth stocks outperformed value, with technology leading sector gains while materials and energy lagged. Investor sentiment remained focused on innovation, though elevated valuations prompted caution.

October 2025 delivered moderate gains across global equity markets. The S&P 500 rose 2.27%, led by mega-cap technology stocks benefiting from strong earnings and AI-driven growth. The Russell 2000 returned 1.76%, continuing its upward trend but underperforming large caps. China’s equity market declined, with the MSCI China Index falling 3.81% due to concerns over export controls and domestic economic softness. Emerging markets gained 3.8%, supported by strong tech performance in South Korea and Taiwan, currency strength, and optimism around industrial AI growth. Growth stocks outperformed value, with technology leading sector gains while materials and energy lagged. Investor sentiment remained focused on innovation, though elevated valuations prompted caution.

The Federal Reserve cut rates by 25 basis points to 4.00%, citing soft labour market data and easing inflation, with headline CPI down to 3.0%. This supported gains in government bonds, with the 10-year Treasury yield falling to 4.08%. Investment-grade and high-yield bonds performed well, and emerging market debt benefited from improving fundamentals and a US dollar that remains under pressure. In the UK, inflation held at 3.8%, and the Bank of England kept rates unchanged at 4.0% amid internal divisions around inflation and growth trajectories.

South Africa

South African financial markets posted mixed results over the month. The FTSE/JSE All Share Index declined by 0.21% in ZAR terms, reflecting a modest pullback from September’s strong gains. Resource stocks, which had led the rally earlier in the year, came under pressure due to softer commodity prices and profit-taking. Financials and industrials showed resilience, with select counters like Naspers and Prosus continuing to post solid returns. Listed property posted a subdued returns this month, after strong rallies seen in August and September.

The South African bond market performed positively, with the 10-year government bond yield falling from 9.18% at the end of September to 8.77% by 31 October, marking a 41 basis point decline. This reflected improved investor confidence, particularly from offshore participants, following stable inflation prints and credible monetary policy developments. The South African Reserve Bank maintained the repo rate at 7.00%, citing contained inflation, which held steady at 3.4%, near the lower bound of the 3%–6% percent target band. Bonds and the Rand remain supported as we move towards the MTBPS in November, which is expected to provide positive updates on an improving fiscal position.

The Iza Portfolios

October 2025 marked the continuation of a vigorous global equity rally, building on the recovery from the April “Liberation Day” sell-off — a geopolitical jolt that had briefly rattled markets. From a sterling investor’s viewpoint, this upswing has been particularly rewarding, amplified by persistent U.S. dollar strength. As of month-end, the MSCI World Index stood 13.9% above its February 2025 peak, prior to the pre-Liberation weakness, and was an impressive 36.3% above the April troughs. This resilience reflects robust corporate earnings, easing inflation signals, and central bank steadiness, though pockets of elevated valuations warrant caution.

The dollar’s dominance has been a tailwind for GBP-based portfolios like ours. Since June 30, 2025, the USD has climbed 4.5% against the pound, enhancing returns on our substantial U.S.-exposed holdings and contributing an extra 1-2% uplift to quarterly performance. This currency dynamic underscores the benefits of global diversification for UK investors, even as it heightens FX sensitivity in a post-Brexit, high-rate environment.

Sector-wise, the rally favored growth themes, with Information Technology, Communication Services, and Consumer Discretionary leading the charge, driven by AI hype, digital ad growth, and resilient consumer spending. In contrast, defensives lagged: Consumer, Health Care, and Real Estate suffered from margin squeezes and rate pressures, highlighting the rotation toward cyclicals in this risk-on phase.

IZA Global Balanced Fund

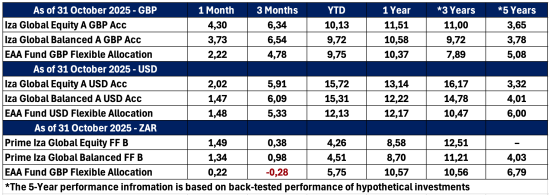

For the Iza Global Balanced Fund, our 72.1% equity allocation captured much of this momentum, delivering a 3.7% monthly return and 9.72% for the year in GBP. Active managers shone, with standouts including the T. Rowe Price Global Focus Equity Fund (fueled by tech disruptors) and Prescient China Balanced Fund (riding Beijing’s stimulus-led rebound in listed firms). These picks validated our tilt toward innovation and emerging recoveries.

Passive anchors, via MSCI World ETFs, provided steady ballast despite lagging our active managers year-to-date; they’ve returned 13.3% in GBP.

Relative underperformers included the Guinness Global Equity Income Fund, whose value- and dividend-focused approach offers longterm stability, and the Nomura High Conviction Global Equity Fund, hampered by consolidation in its concentrated basket of quality names like Microsoft, Alphabet, Amazon, Mastercard, and Nvidia. Both remain vital for balance.

The Iza segregated mandate adds stability through a wide spread of exposures to global bonds and currencies on attractive real yields. This portfolio continues to be a strong contributor to returns despite the recent dollar strength.

Rounding out the highlights, our gold allocation of 3.9% of the portfolio was the standout, surging 44.7% year-to-date in GBP. In a landscape of macroeconomic flux (e.g., U.S. election risks, Middle East tensions) and geopolitical crosswinds, this holding has slashed volatility while boosting Sharpe ratios, proving its worth as a true diversifier.

Looking forward, with U.S. rates likely declining and UK growth forecasts at 1.2% for 2026, we favor selective growth exposure tempered by defensives The fund targets 8 10% annualized GBP returns with controlled drawdowns.

Iza Global Equity Fund

For the Iza Global Equity Fund, our allocation captured much of this momentum, delivering a 4.3% monthly return and 10.12% for the year in GBP. Active managers shone, with standouts including the T. Rowe Price Global Focus Equity Fund (fueled by tech disruptors) and Prescient China Balanced Fund (riding Beijing’s stimulus-led rebound in listed firms). These picks validated our tilt toward innovation and emerging recoveries.

Passive anchors, via MSCI World ETFs, provided steady ballast despite lagging our active managers year-to-date; they’ve returned 13.3% in GBP.

Relative underperformers included the Guinness Global Equity Income Fund, whose value- and dividend-focused approach offers long-term stability, and the Nomura High Conviction Global Equity Fund, hampered by consolidation in its concentrated basket of quality names like Microsoft, Alphabet, Amazon, Mastercard, and Nvidia. Both remain vital for balance.

Quote of the month

Know what you own, and know why you own it.

Peter Lynch

Funds’ Performance Summary

Asset Class Performance (Base Currency)