Click the image to read the PDF

Click the button to download the PDF

Local Commentary

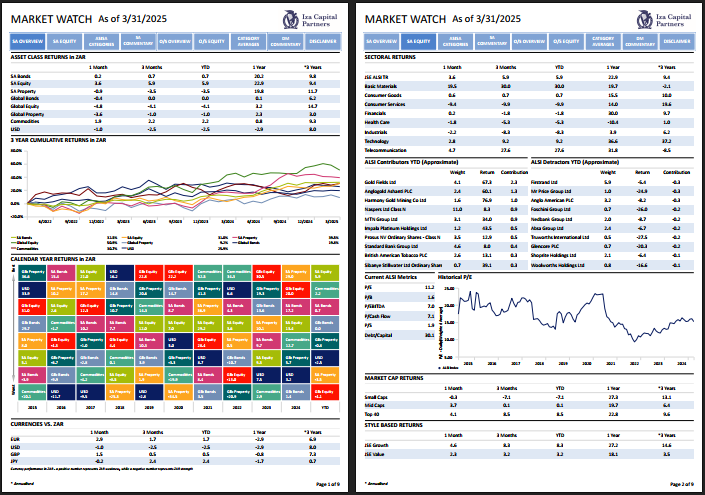

March closed out the first quarter on a constructive note for local investors, with the FTSE/JSE All Share Index returning +3.6% for the month and +5.9% year-to-date. However, while headline performance was encouraging, it masked a bifurcated market beneath the surface. Gains were overwhelmingly concentrated in the mining sector, particularly among gold and platinum group metal (PGM) counters, while the broader equity market saw muted to negative returns in aggregate.

Gold miners delivered extraordinary returns, gaining 33% in March and 68% for the year to date, as the gold price surged past the US$3,000/oz level—a milestone that would have seemed ambitious just 18 months ago when the metal traded near US$1,800/oz. Platinum miners followed closely, posting gains of 40% in the month and 37% year to date. The rally was fuelled by a combination of geopolitical uncertainty, declining real yields, and sustained central bank buying—especially from emerging market central banks. Rhodium, a key PGM, also surged 21% in March, adding further tailwind to PGM-heavy portfolios. While precious metals supported the index-level gains, performance across other sectors was far less impressive. Many industrials and financials struggled to gain traction, a sign of lingering caution among investors amid concerns around growth, fiscal policy, and global risk appetite.

Despite a generally subdued backdrop outside of mining, several large caps stood out. Standard Bank advanced 8% in March, buoyed by a solid set of fullyear results. The bank reported a 4% year-on-year increase in headline earnings per share, in line with expectations.

Sun International also had a strong month (+9%), driven by resilient earnings and growing investor optimism around its digital strategy. While overall earnings growth for 2024 came in at a modest 3% YoY, the standout was a 60% year-on-year surge in online gambling revenue.

On the other end of the performance spectrum, private education group Curro saw its share price tumble 28% during the month. The company’s results pointed to continued operational inefficiencies, with poor occupancy rates and slowing enrolment figures suggesting a more protracted turnaround than investors had hoped for.

From a macro perspective, South Africa’s inflation dynamics remain encouraging. Core CPI came in at 3.4% year-on-year—slightly below consensus estimates of 3.5%—marking continued disinflation and a move deeper into the lower half of the SARB’s target range (3%–6%). Food price inflation has remained contained, and fuel base effects have become less pronounced, reducing pressure on headline inflation metrics.

Despite the subdued inflation environment, the South African Reserve Bank opted to hold the repo rate steady at 7.5%. This leaves the prime lending rate unchanged at 11%, approximately 150 basis points above its 15-year average. The central bank’s decision was informed by persistent risks to the inflation outlook, including potential currency volatility and exogenous shocks. Market expectations still point to potential easing later in 2025, provided inflation continues to moderate and global monetary conditions become more supportive.

On the fixed income side, the SA government’s 10-year bond yield remained steady at 10.6%, broadly unchanged for the month. US Treasury yields were similarly flat, with the US 10-year yield ending March at 4.2%. Stability in global rates provided some relief for emerging market debt, although sentiment remains highly sensitive to global growth revisions and US Federal Reserve rhetoric.

The rand performed relatively well during March, strengthening 2% against the US dollar and 2.8% year-to-date. The recovery was largely driven by a weaker dollar and improving investor sentiment toward emerging markets. However, structural risks—such as load shedding, fiscal uncertainty, and South Africa’s geopolitical positioning—remain key considerations for currency stability going forward.

As we move into the second quarter, investors must navigate a complex environment marked by mixed signals. On one hand, disinflation, relatively high real rates, and a stable currency support the case for policy easing and improved investor sentiment. On the other hand, concentration risk in equity market performance, subdued domestic growth, and ongoing geopolitical uncertainties warrant caution.

Encouragingly, South Africa has made further progress on its FATF greylist commitments, with improvements noted in four of the six outstanding action items. Should the remaining hurdles be cleared, a potential delisting in October 2025 could serve as a catalyst for renewed capital flows and broader risk appetite.

While commodity sectors continue to dominate short-term performance, long-term returns will hinge on disciplined diversification and bottom-up stock selection.

Offshore Commentary

The onset of 2025 has been marked by significant market volatility, a trend that appears poised to persist in the coming quarters. At the year’s inception, prevailing consensus anticipated that the new Republican administration’s “America First” policies would bolster U.S. exceptionalism, further propelling U.S. stocks ahead of their global counterparts. Conversely, these policies were expected to pose challenges for international economic growth.

Contrary to these expectations, the unfolding narrative has diverged. The U.S. administration’s aggressive tariff implementations have heightened uncertainty, dampening domestic growth projections. In contrast, Europe has responded with robust fiscal measures, exceeding many forecasts.

This evolving landscape has seen emerging market equities outperform developed markets, with Chinese and Korean stocks showing notable strength. Value stocks have surpassed growth stocks, while small-cap companies have lagged, returning -3.6%, as escalating trade uncertainties have raised concerns about both slowing growth and rising inflation. Commodities have emerged as top performers this quarter, highlighted by a 19% surge in gold prices.

In the bond markets, increasing recession fears have led to a 2.9% return from U.S. Treasuries. Conversely, in Europe, anticipations of increased issuance to fund expansive government spending have pressured sovereign bonds, with German Bunds declining by 1.6%. Japanese government bonds have notably underperformed, down 2.4%, amid mounting inflationary signals.

Throughout the first quarter, U.S. equity markets have been unsettled by tariff-related developments. Following the imposition of new tariffs on imports from Mexico, Canada, and China in February, March witnessed additional levies on steel, aluminum, and automobiles. The administration’s unpredictable trade stance has led to fluctuating market sentiment, with investors closely monitoring indicators of potential economic deceleration, such as declining capital expenditure intentions reflected in small business surveys.

Amid this heightened uncertainty, the Federal Reserve opted to maintain current interest rates during the quarter. Chair Jerome Powell signalled openness to potential rate cuts in future meetings, indicating the Fed’s increased concern over downside growth risks relative to inflationary pressures. Consequently, U.S. 10-year Treasury yields concluded the quarter at 4.2%, a decrease of 36 basis points since January.

The administration’s confrontational trade policies have galvanized European leaders into action. European Commission President Ursula von der Leyen proposed nearly €800 billion in spending to enhance the bloc’s defense capabilities, combining €150 billion in new European borrowing with €650 billion allocated for increased national defense expenditures within EU fiscal guidelines.

Germany’s anticipated chancellor, Friedrich Merz, has also signalled a departure from fiscal conservatism, proposing reforms to the debt brake to accommodate defense spending and unveiling a €500 billion infrastructure initiative. These announcements have led to a significant uptick in 10-year German Bund yields, which rose over 30 basis points following the news, while equity markets responded positively, with Germany’s DAX Index recording its strongest first quarter since 2023.

The European Central Bank has expressed support for these fiscal initiatives, with President Christine Lagarde commending the proactive approach. The ECB implemented two interest rate cuts during the quarter, with markets anticipating an additional 60 basis points in reductions by year’s end.

In the UK, fiscal challenges culminated in Chancellor Rachel Reeves announcing £8.4 billion in spending cuts to adhere to fiscal rules. Despite these austerity measures, UK assets remained relatively stable, with 10-year Gilt yields rising modestly by 10 basis points and equities outperforming many international peers year-to-date.

Asian equity markets exhibited considerable dispersion during the quarter. Chinese equities advanced by 15%, driven by less severe-than-anticipated U.S. tariffs, renewed optimism in the tech sector following DeepSeek’s AI advancements, and indications of supportive policies from Beijing. In contrast, Indian equities declined by 2.9%, while Japanese markets faced headwinds from a strengthening yen, resulting from narrowing interest rate differentials.

Despite the looming threat of tariffs, strong corporate fundamentals have mitigated spread widening in U.S. credit markets. European credit returns were impacted by movements in local government bonds; however, investment-grade spreads narrowed over the quarter. A weaker U.S. dollar provided a tailwind for emerging market debt, while a significant decline in U.S. real yields allowed inflation-linked bonds to outperform their nominal counterparts.

The tumultuous start to 2025 underscores the likelihood of continued volatility as markets adjust to dynamic policy shifts. For investors, the efficacy of a diversified approach has become evident, contrasting with the concentrated markets that posed challenges in 2024. This quarter demonstrated the balancing effect between stocks and bonds, with declining U.S. yields offsetting equity losses, and vice versa in Europe. Within equities, diversification across regions and sectors has proven advantageous, equipping investors with the tools necessary to navigate the uncertain terrain ahead.