Our report is available below

Click the image to view/download the PDF

Market Insights

The first quarter of 2025 reminded investors that markets don’t move in straight lines, and neither do geopolitics. After years of U.S. outperformance, markets have entered a new regime shaped by trade wars, shifting fiscal priorities, and renewed global dispersion.

The first quarter of 2025 reminded investors that markets don’t move in straight lines, and neither do geopolitics. After years of U.S. outperformance, markets have entered a new regime shaped by trade wars, shifting fiscal priorities, and renewed global dispersion.

The quarter began with hopes that Donald Trump’s return to the White House would unleash another wave of tax cuts and deregulation. Instead, the world got tariffs. From steel and aluminium to autos and tech, the U.S. administration has reintroduced broad-based protectionist policies. These have not only spooked domestic growth expectations but also prompted a counter-punch from Europe in the form of €800 billion in defence and infrastructure spending.

The result: a highly volatile but telling quarter. U.S. equities wobbled, European and Chinese equities surged, and commodities (especially gold) soared, driven by inflation fears and geopolitical anxiety. Most notably, the MSCI World Index fell -6.8% in GBP in March alone, finishing Q1 down -4.8%, a sobering shift for anyone relying on passive cap-weighted exposure alone.

Meanwhile, bonds reasserted their value as portfolio stabilizers, particularly in the U.S., where Treasury yields dropped by 36bps and supported strong price gains. European sovereign bonds struggled, reflecting the anticipated debt burden of new fiscal packages, while emerging market credit held up surprisingly well on the back of a softer dollar and stable fundamentals.

At Iza, our focus on diversification across styles, asset classes, and regions continued to bear fruit. While no portfolio is immune to market drawdowns, both the Iza Global Equity and Balanced Funds outperformed the MSCI World Index in Q1, and performance relative to peers has been equally strong. As of April 8, before the 90-day tariff truce bounce, the Iza Balanced Fund was firmly top quartile both MTD and YTD versus ASISA Global Flexible Peers.

South Africa

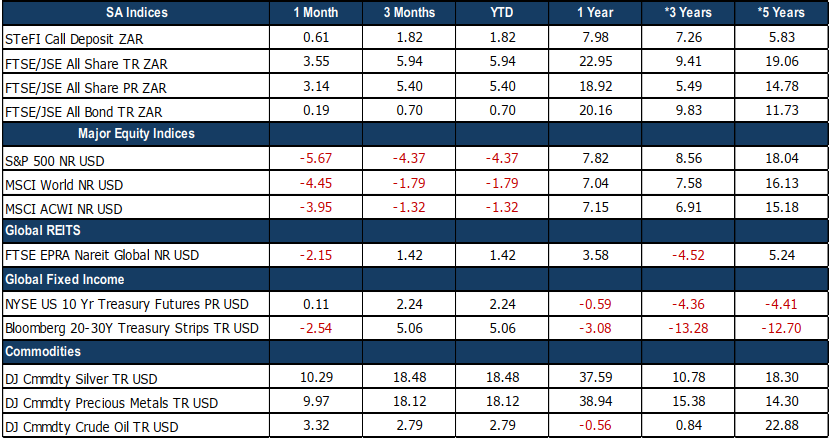

March closed out the first quarter on a constructive note for local investors, with the FTSE/JSE All Share Index returning +3.6% for the month and +5.9% year-to-date. However, while headline performance was encouraging, it masked a bifurcated market beneath the surface. Gains were overwhelmingly concentrated in the mining sector, particularly among gold and platinum group metal (PGM) counters, while the broader equity market saw muted to negative returns in aggregate.

Gold miners delivered extraordinary returns, gaining 33% in March and 68% for the year to date, as the gold price surged past the US$3,000/oz level—a milestone that would have seemed ambitious just 18 months ago when the metal traded near US$1,800/oz. Platinum miners followed closely, posting gains of 40% in the month and 37% year to date. The rally was fuelled by a combination of geopolitical uncertainty, declining real yields, and sustained central bank buying— especially from emerging market central banks. Rhodium, a key PGM, also surged 21% in March, adding further tailwind to PGM-heavy portfolios.

While precious metals supported the index-level gains, performance across other sectors was far less impressive. Many industrials and financials struggled to gain traction, a sign of lingering caution among investors amid concerns around growth, fiscal policy, and global risk appetite.

Despite a generally subdued backdrop outside of mining, several large caps stood out. Standard Bank advanced 8% in March, buoyed by a solid set of full-year results. The bank reported a 4% year-on-year increase in headline earnings per share, in line with expectations.

From a macro perspective, South Africa’s inflation dynamics remain encouraging. Core CPI came in at 3.4% year-onyear—slightly below consensus estimates of 3.5%—marking continued disinflation and a move deeper into the lower half of the SARB’s target range (3%–6%). Food price inflation has remained contained, and fuel base effects have become less pronounced, reducing pressure on headline inflation metrics.

Despite the subdued inflation environment, the South African Reserve Bank opted to hold the repo rate steady at 7.5%. This leaves the prime lending rate unchanged at 11%, approximately 150 basis points above its 15-year average. The central bank’s decision was informed by persistent risks to the inflation outlook, including potential currency volatility and exogenous shocks. Market expectations still point to potential easing later in 2025, provided inflation continues to moderate and global monetary conditions become more supportive.

On the fixed income side, the SA government’s 10-year bond yield remained steady at 10.6%, broadly unchanged for the month. US Treasury yields were similarly flat, with the US 10-year yield ending March at 4.2%. Stability in global rates provided some relief for emerging market debt, although sentiment remains highly sensitive to global growth revisions and US Federal Reserve rhetoric.

The rand performed relatively well during March, strengthening 2% against the US dollar and 2.8% year-to-date. The recovery was largely driven by a weaker dollar and improving investor sentiment toward emerging markets. However, structural risks—such as load shedding, fiscal uncertainty, and South Africa’s geopolitical positioning—remain key considerations for currency stability going forward.

As we move into the second quarter, investors must navigate a complex environment marked by mixed signals. On one hand, disinflation, relatively high real rates, and a stable currency support the case for policy easing and improved investor sentiment. On the other hand, concentration risk in equity market performance, subdued domestic growth, and ongoing geopolitical uncertainties warrant caution.

The Iza Portfolios

IZA Global Balanced Fund

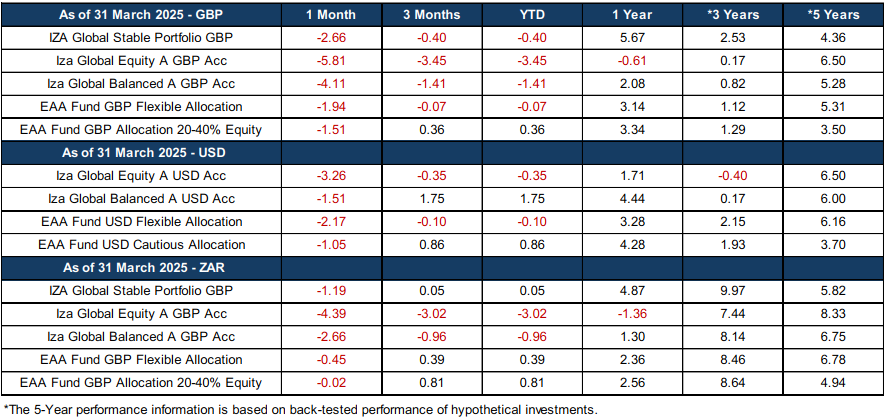

The Iza Global Balanced Fund returned -1.41% for the quarter, outperforming is ASISA Global Flexible peers and the MSCI World Index’s – 4.8% decline in GBP. Despite a temporary slip into the third quartile vs the EAA Global Flex GBP category in March (largely due to a GBP/USD currency bias in that group), the Fund remains top quartile over two years and maintains a consistent position in the top quartiles’ vs USDbased peers. That’s no accident, it’s the result of carefully constructed exposures that match the global nature of most investor objectives. Gold was the hero of the quarter. The Fund’s position in SPDR Gold Trust gained +15.3%, driven by risk aversion, rising real rates volatility, and surging safe-haven demand. On the income side, U.S. Treasuries (+0.37%) and Rubrics Enhanced Yield (+1.07%) provided steady performance as bond yields fell and volatility rose.

On the equity front, Berkshire Hathaway again proved its worth, gaining +13.84% and offering investors classic value exposure, strong balance sheet protection, and Buffett’s growing cash war chest. Dodge & Cox added further resilience with +2.88%, while Guinness Global Equity Income (-0.52%) remained a stabilizer, outperforming most quality peers.

Some of the Fund’s growth and quality names like T. Rowe Price, Nomura, lagged the MSCI world reflecting style pressures in Q1. After several calls with each of these managers to understand the drivers, we believe this to be more short term and already seeing both managers recover vs the MSCI World in April. Importantly, both the underlying fund managers have continued to outperform peers in the longer term. These are names that have demonstrated consistent alpha through cycles.

Perhaps most importantly, our inclusion of Prescient China Balanced in early February couldn’t have been better timed. After a deep dive and in-person DD process in Shanghai, we added this high-quality, dynamic fund to both Iza Balanced and Equity. Despite the noise, it delivered better returns than Chinese equity benchmarks like the CSI 300, and its flexible, diversified exposure to AI, semiconductors, and consumer sectors already helped soften the blow in March. The benefits have accelerated further into April. This addition has also improved our jurisdictional diversification now essential as Trump’s tariffs begin to splinter global markets.

Iza Global Equity Fund:

The Iza Global Equity Fund returned -3.45% in Q1, ahead of the MSCI World Index’s -4.8% GBP loss, and with additional outperformance extending into April by a further 2% come the 8th of April. While March was tough (-5.81%) our diversification meant the Fund was still ahead of the 6.8% fall of the MSCI World Index. Berkshire Hathaway was again a standout, rising +13.84%, benefiting from a stellar annual letter, strong Q4 earnings, and disclosures of record cash reserves. With high-quality names coming under pressure, investors gravitated to Berkshire’s defensive blend of insurance, rails, and massive cash optionality.

Dodge & Cox (+2.88%) added solid value, continuing to benefit from the global rotation into value and cyclicals. Guinness Global Equity Income (-0.52%) remained one of the best quality-dividend performers globally, while Clearance Camino having struggled to start the year lost half of what the market did in March and helped hedge some of the real asset risks, we flagged last year and capturing some of the rotation away from pure US based assets.

As pointed out above Nomura, T. Rowe, and Guinness Global Innovators struggled given the rotation to more value orientated stocks during the quarter.

The Fund’s timely inclusion of Prescient China Balanced (-3.23%) was a differentiator. Despite Chinese equity benchmarks falling sharply in March, this fund’s unique construction holding over 200 names and using a rules-based equity allocation, allowed it to outperform the CSI 300, Hang Seng and broader global equity markets, while delivering a stabilizing force to the portfolio. The inclusion also expands our Asia AI exposure and aligns with our view that China and the U.S. will remain the two poles of innovation in a decoupling world.

Conclusion: Built for Balance, Positioned for Opportunity

If 2024 was a test of endurance amid narrow market leadership, Q1 2025 has tested investors’ preparedness for genuine dispersion, between regions, sectors, styles, and policy approaches. The Iza Funds continue to embrace this complexity.

By combining active manager selection, style diversification, and a forward-looking geographic lens, we’ve been able to protect capital, outperform benchmarks, and most importantly, build resilience into our clients’ portfolios. This is of paramount importance given what Trump unleashed in April. Markets are experienced a sharp repricing the size and speed of which are unprecedented, but one that we knew could quickly shift if policy rhetoric softens and has taken place just in the last 24 hours with the S&P 500 staging its biggest one-day gain since 2008. While it’s impossible to predict the next headline, we are not sitting still. We’re engaging daily with our underlying managers, actively monitoring portfolio risks, and prepared to act if needed.

Given how fresh and fast-moving these developments are, we’re still working closely with managers to fully assess the impact and changes being undertaken if any. These are the moments where clear strategy beats noisy headlines.

Trump’s Tariff Turmoil Update:

President Trump’s announced sweeping tariffs on 2 April, global markets have endured a fortnight of policy-induced chaos. We’ve seen violent market swings, sharp bond yield drops, spikes, and a series of contradictory policy announcements that have sown uncertainty across the global financial system. Despite this, our decision to remain calm and disciplined. anchored by robust diversification and deep engagement with global managers has proven both prudent and profitable. While others reacted emotionally to headlines, we focused on the underlying trends and held our course, helping our client funds/portfolios remain top performers vs peers.

Bond Market Stress & Political Capitulation

The bond market proved to be the most telling and decisive voice during this chaotic stretch. What began as a brief flight to safety quickly gave way to a sharp and sustained sell-off in Treasuries. Investors were rattled by a trifecta of risks: widening fiscal deficits, inflationary pressures from tariff-induced import costs, and speculation that key foreign buyers, particularly China, were scaling back Treasury purchases. Hedge fund liquidations of leveraged bond positions further destabilized markets, pushing the 10-year yield from 4.18% to 4.61% in just over a week. This sudden spike in yields placed enormous pressure on the administration. Faced with a looming self-inflicted recession and midterm elections on the horizon, Trump was forced to retreat from his all-out tariff stance. But the nature of this reversal, midnight announcements, walk-backs, and inconsistent language, only compounded market uncertainty. With his political capital eroding and voter anger building, it’s clear that self-preservation, not economic logic, is shaping the path forward.

Our Strategy: Insight Over Instinct

Amid the chaos, our investment philosophy remained grounded in foresight, discipline, and high-quality information. We drew on direct communication with leading managers in the U.S. and China and coupled that with real-time geopolitical intelligence from our offshore experts. This gave us an edge, allowing us to anticipate that the economic damage would likely force a policy reversal and that making emotionally driven portfolio changes would be counterproductive. Moreover, our diversified portfolio construction, across regions, asset classes, and risk profiles helped us navigate the storm more effectively than many peers. While others were blindsided by the swings, our positioning allowed us to weather the worst and take advantage of mispricing’s without overreacting to noise.

Looking Ahead: More Volatility, More Opportunity

Despite the temporary consumer electronics exemption, the picture is far from clear. Trump’s latest reversal makes it evident that volatility will persist. With semiconductor and pharmaceutical tariffs now firmly on the agenda and China holding its line, there is no easy exit from this trade war.

Markets will remain sensitive to every tweet, press conference, and policy leak. Bond yields are still elevated, inflation fears are lingering, and global supply chains are reassessing exposure. Importantly, Trump’s credibility has taken a hit, and with midterms fast approaching, his next moves are likely to be politically not economically motivated.

Quote of the month

See the investment world as an ocean and buy where you get the most value for your money.

John Templeton

Funds’ Performance Summary

Asset Class Performance (Base Currency)