Our report is available below

Click the image to view/download the PDF

Market Insights

In June 2025, U.S. equity markets soared to record highs, powered by robust tech and AI stocks, improved corporate earnings, and easing trade frictions. The S&P 500 gained nearly 5% and the Nasdaq Composite rose over 6%, both reaching new all-time highs. Key economic indicators, including jobs and inflation data, were closely watched, alongside a pivotal Federal Reserve rate meeting. However, investor sentiment was tempered by fiscal uncertainty as Congress debated key budget and tariff measures. In the UK, the FTSE 100 remained stagnant, reflecting economic caution, while the Bank of England held interest rates steady amid divided opinions and modest improvements in inflation and employment. The new Labour government introduced a comprehensive spending review focused on essential public services. Trade tensions persisted, with the U.S. maintaining steep tariffs on Chinese goods despite a partial trade agreement, and new tariffs targeting steel appliances and copper imports. Globally, improved trade relations lifted sentiment, especially in the U.S. and Asia. Meanwhile, a dramatic escalation in the Iran-Israel conflict, with airstrikes and missile exchanges, disrupted Middle Eastern energy supplies, spiked oil prices, and heightened market volatility, prompting investors to seek safe-haven assets.

In June 2025, U.S. equity markets soared to record highs, powered by robust tech and AI stocks, improved corporate earnings, and easing trade frictions. The S&P 500 gained nearly 5% and the Nasdaq Composite rose over 6%, both reaching new all-time highs. Key economic indicators, including jobs and inflation data, were closely watched, alongside a pivotal Federal Reserve rate meeting. However, investor sentiment was tempered by fiscal uncertainty as Congress debated key budget and tariff measures. In the UK, the FTSE 100 remained stagnant, reflecting economic caution, while the Bank of England held interest rates steady amid divided opinions and modest improvements in inflation and employment. The new Labour government introduced a comprehensive spending review focused on essential public services. Trade tensions persisted, with the U.S. maintaining steep tariffs on Chinese goods despite a partial trade agreement, and new tariffs targeting steel appliances and copper imports. Globally, improved trade relations lifted sentiment, especially in the U.S. and Asia. Meanwhile, a dramatic escalation in the Iran-Israel conflict, with airstrikes and missile exchanges, disrupted Middle Eastern energy supplies, spiked oil prices, and heightened market volatility, prompting investors to seek safe-haven assets.

UK inflation eased slightly to 3.4% in May 2025 from 3.5% in April, matching expectations, with the slowdown mainly due to falling transport costs—especially cheaper airfares—and a correction of a previous tax data error. However, food prices picked up sharply, contributing to the first rise in overall retail prices since July 2024. Core inflation, which excludes more volatile items, also moderated to 3.5% from 3.8% the previous month. The Bank of England kept its interest rate at 4.25% in June but signalled that inflation may climb again later in the year as higher labour and household costs feed through. Transport and housing costs exerted downward pressure, while food, furniture, and household goods pushed inflation up, and rising oil prices remain a risk for future inflation.

The US dollar continued to lose ground in June 2025, falling about 1.5% for the month and bringing its year-to-date decline to over 10% against a basket of major currencies—its worst first-half performance since 1973. This persistent weakness was fuelled by uncertainty over US fiscal policy, mounting government debt, and rising expectations that the Federal Reserve will cut interest rates later in the year. Although there were brief periods of stabilization following strong economic data, the overall trend remained downward, and analysts expect the dollar to face ongoing challenges in the near future. In June 2025, both the euro and the pound appreciated against the US dollar. The euro climbed from roughly $1.14 at the start of the month to nearly $1.18 by June’s end, reaching its highest point of the year and averaging about $1.15 throughout June. This upward movement was mainly due to the dollar’s broad weakness and steady economic performance in Europe. The British pound also advanced versus the dollar, mirroring the euro’s gains, as stable UK monetary policy and the softening dollar supported its strength.

China’s stock market recorded moderate gains in June 2025, with the Shanghai Composite Index rising about 3.2% for the month and nearly 19% year-on-year. This improvement was underpinned by signs of stabilizing consumer demand—June saw the first positive inflation reading in five months—and continued government support for technology and AI sectors. Despite these gains, challenges persisted: producer prices fell sharply, indicating weak industrial demand, and domestic consumption remained soft. Trade tensions with the US also weighed on sentiment, as Beijing warned of possible retaliation if tariffs were reimposed. Market performance was mixed, with mainland A-shares largely flat while Hong Kong-listed Chinese stocks saw stronger advances, reflecting greater foreign investor interest and successful IPOs.

South Africa

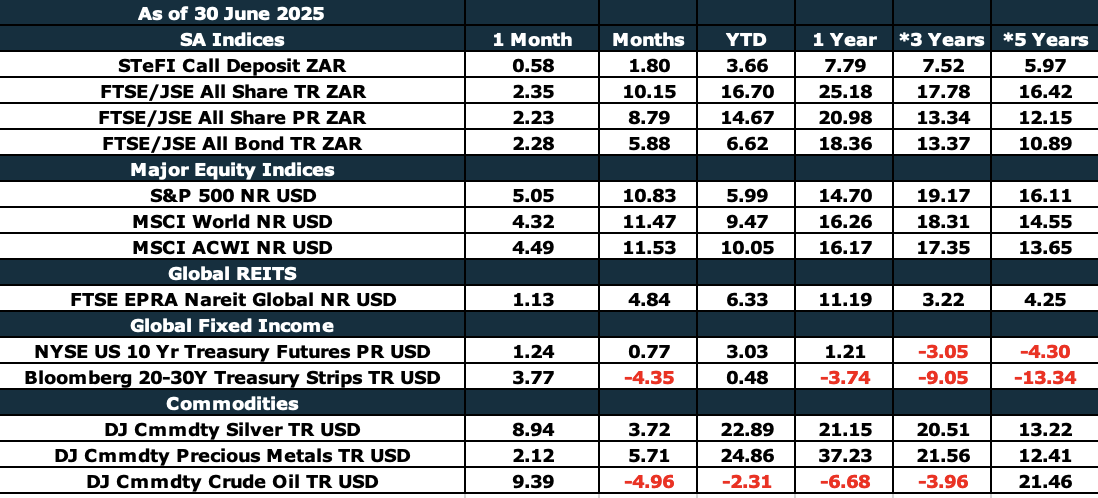

Global risk assets continued their upward trajectory in June, despite heightened geopolitical uncertainty following escalating Middle East tensions. While global equity markets shrugged off early volatility and rallied on strong tech earnings and AI-driven optimism, the local South African market responded with resilience of its own—supported by a surge in resource stocks and favourable inflation dynamics.

South African equities climbed 2.4% in June, underpinned by a 4.8% surge in resource stocks. Platinum was the standout, rallying 26.2%—its largest monthly gain in over three decades—driven by signs of constrained supply, auto-sector restocking, and speculative positioning amid Middle East supply risks. Key beneficiaries included Northam Platinum, Impala, and Sibanye-Stillwater, all of which posted double-digit gains.

The FTSE/JSE All Share Index is now up 16.7% year-to-date, with resources accounting for the bulk of that advance (+46.8% YTD for the Resource 20 Index). Industrials also posted a solid 2.4% return, led by defensives and exporters, while financials (+0.8%) underperformed, weighed down by bank and life insurance counters. Notably, the retail sector remained under pressure, falling 5.3% in June and extending its year-to-date loss to 16.7%—a puzzling underperformance in light of easing inflation, falling rates, and additional consumer liquidity from pension withdrawals.

Headline inflation remained unchanged at 2.8% year-on-year in May, marking the third consecutive month below the SARB’s 3–6% target range. Core inflation held steady at 3.0%, slightly below expectations. The largest disinflationary force remained transport, where y/y prices fell by nearly 15% due to ongoing declines in fuel costs.

However, food inflation accelerated to 4.4%, driven by rising meat prices—exacerbated by a foot-and-mouth disease outbreak and elevated feed costs. Encouragingly, producer inflation for food eased during the month, suggesting CPI pressures from food may be close to peaking.

South African bonds continued to rally in June, with the All-Bond Index gaining 2.3%. The yield curve bull-flattened for a second consecutive month, as investor attention remained fixed on the SARB’s evolving inflation-targeting framework and its implications for long-term yields. The benchmark 10-year bond yield fell nearly 20 basis points, touching a three-year low intra-month.

Contributing to this strength was the global bond rally, with U.S. 10-year Treasury yields falling 17bps as softening inflation prints raised expectations for a pause by the Fed. Domestically, the improving terms of trade and stable fiscal signals also supported sentiment.

Inflation-linked bonds underperformed (+0.6%), reflecting subdued inflation and thin liquidity. The market remains wary of potential oversupply in this segment should Treasury adjust its issuance mix, particularly in the absence of primary dealers and amid poor secondary market liquidity. The listed property sector saw a mild pullback in June, declining by 0.9%, although year-to-date performance remains positive at +5.3%. Sentiment was weighed down by concerns over higher long-bond yields in global markets, as well as valuation fatigue after a strong first half.

The rand appreciated by 1.6% against the U.S. dollar, continuing its trend of strength seen over the quarter. This was aided by a weaker dollar environment and rising commodity prices—particularly platinum, copper (+6.0%) and coal (+9.0%). Oil prices were volatile, initially rising on Middle East tension but retreating later in the month. Brent closed up 6.3%. First-quarter GDP data, released in June, confirmed the fragility of South Africa’s recovery. The economy expanded just 0.1% quarter-on-quarter, with gains in agriculture (+15.5%) and transport (+2.4%) offset by declines in mining (-4.1%) and manufacturing (-2.0%).

Despite an uncertain global backdrop, local asset classes continued to deliver solid performance in June. While the resource-led rally and improving inflation dynamics provide tailwinds, the underlying economy remains weak, and risks around fiscal reform and load-shedding persist. As the second half of 2025 unfolds, much will depend on clarity around the SARB’s inflation target review, Treasury’s issuance strategy, and the strength of the consumer recovery. In this environment, selectivity across sectors and active portfolio positioning remains critical.

The Iza Portfolios

IZA Global Balanced Fund

The IZA Global Balanced Fund delivered a solid performance in USD in June 2025, and on a year-to-date. The fund returned 8.7% year-to-date in USD and 3.2% on a month-to-date (net of fees) and has outperformed the benchmark (EAA Global Flexible) on a YTD and MTD basis. The June performance was supported by diversified exposure to global equities, fixed income and structured products, with significant holdings in North America and Europe. The fund’s strategy of blending value, quality, and growth styles helped it outperform peers during periods of market volatility and capture the upside and generate significant alpha as compared to peers. With the dollar continuing to weaken, we decided to rotate the cash in EUR and GBP to limit the downside on the currency exposures. The fund delivered a net return of 1.16% in GBP. The pound’s strength against the dollar and euro in June 2025 reduced the value of overseas earnings and dividends for UK investors, which weighed on returns. At the same time, declining company profit forecasts, record government borrowing, policy uncertainty, and concerns over potential US tariffs contributed to a cautious investment climate, keeping UK equity and security returns subdued for the month.

Iza Global Equity Fund

The IZA Global Equity Fund equally delivered a very pleasing USD return of 3.92% for the month and 8.72% for the year. In June 2025, UK and European property markets outperformed due to strong demand, especially in more affordable regions. Although UK asking prices fell slightly because of increased supply and higher stamp duty effects, actual sales prices and volumes remained solid outside London and the South East. Flexible lending criteria also helped boost mortgage approvals. Similar positive trends in Europe, supported by rising wages and buyer confidence, contributed to steady property market performance. The robust demand in lower-priced areas drove property markets to outperform other asset classes this month.

Growth stocks within the portfolio saw gains fuelled by rising investor optimism about the economic outlook, impressive results from leading tech firms, and confidence that companies could manage higher tariff-related costs. Supportive factors included easing trade tensions, solid corporate earnings, and expectations that the US Federal Reserve might adopt a more accommodative stance. This environment helped US growth indices like the S&P 500 and Nasdaq reach new highs. Meanwhile, increased business activity, fiscal stimulus, and stable politics in Europe and the UK also lifted sentiment, allowing growth sectors to outperform across major markets.

Key Performance Highlights across both funds

Contributors across both funds:

In June 2025, Scottish Mortgage delivered a strong return of 5.30% and 8.55% on a year-to-date basis. Scottish Mortgage Investment Trust performed strongly in June 2025, driven by its focus on high-growth technology and innovative companies that showed resilient earnings despite tariff-related risks. Key contributors included major tech firms from the US and Asia, as well as private companies in AI, healthcare, and green technology sectors. The trust’s long-term, global investment strategy allowed it to capitalize on innovation trends and digital transformation, helping it outperform amid ongoing trade uncertainties and market volatility.

T. Rowe delivered a MTD performed of 4.01% in GBP which was hugely attributable to broad gains in global stock markets, especially outside the US. The fund benefited from careful selection of companies with solid, sustainable growth in both developed and emerging markets. Its diversified portfolio helped reduce the impact of tariff concerns, while strong performance in technology, healthcare, and consumer sectors further boosted returns.

The MSCI World Index delivered moderate returns (2.39% in GBP for the month) compared to other equity funds in June 2025 because its broad exposure across various regions and sectors balanced strong performers with weaker ones, limiting overall gains. Concerns about tariffs, global economic growth, and currency fluctuations weighed on some components, further moderating returns. While the index posted positive results, its diversified and fixed allocation led to more subdued performance compared to more focused equity funds.

The Guinness Global Innovators Fund added to its gains due to its exposure to technology and innovation-driven companies. Top holdings such as Nvidia, Intuit, Infineon, and TSMC posted strong earnings and benefited from enthusiasm around AI and digital transformation. Supportive market conditions and resilient, high-quality portfolio companies enabled the fund to deliver stronger returns than broader indices.

The Dodge & Cox Stock Fund gained in June 2025, with its value increasing steadily and showing strong year-to-date and long-term performance compared to peers. Its success is attributed to a focus on value stocks, a well-diversified portfolio across various sectors, and effective risk management strategies that enhance resilience during market fluctuations.

Detractors in the IZA Global Balanced Fund:

Gold prices dipped slightly in June 2025 as investors took profits after earlier highs and expectations for slow US interest rate cuts reduced demand. Easing Middle East tensions also lessened gold’s appeal as a safe haven. However, the outlook remains positive due to ongoing tariff risks, geopolitical uncertainty, and strong central bank buying.

Prescient China delivered moderate returns in June – primarily because Chinese equities fell in June 2025 due to renewed US trade tensions, weak domestic economic data, and persistent concerns about low consumer demand and industrial deflation. Limited impact from government stimulus and cautious investor sentiment also contributed to the market’s decline.

Our Bond holdings achieved moderate gains as softer economic data and low inflation, especially in China where the 10-year government bond yield dropped to around 1.64%, led to lower yields and higher bond prices. Central banks provided liquidity support, while ongoing economic uncertainty, deflation concerns, and challenges in sectors like real estate increased demand for safe-haven assets. Strong technical factors, such as robust local bank demand and reinvestment flows from maturing bonds, further supported bond markets despite global trade tensions and subdued credit demand.

Quote of the month

Courage taught me no matter how bad a crisis gets … any sound investment will eventually pay off.

Carlos Slim Helu

Funds’ Performance Summary

Asset Class Performance (Base Currency)